Crypto Basis Trading: A Complete Guide

Complete guide to Crypto Basis Trading. Learn the delta-neutral spot/perp strategy for funding yield. Avoid manual errors. Use automation.

Crypto Twitter is often abuzz with talk of eye-popping APRs earned from funding rates. You see screenshots, celebratory posts, and maybe you've wondered: is this some kind of magical free lunch only the degens know about?

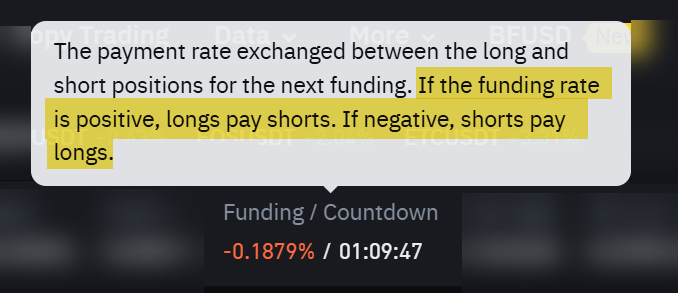

Perpetual futures contracts sometimes trade at a different price than the underlying crypto asset (the "spot" price), and mechanisms exist to keep these prices relatively aligned. One key mechanism is the funding rate, where traders on one side of the contract periodically pay traders on the other side.

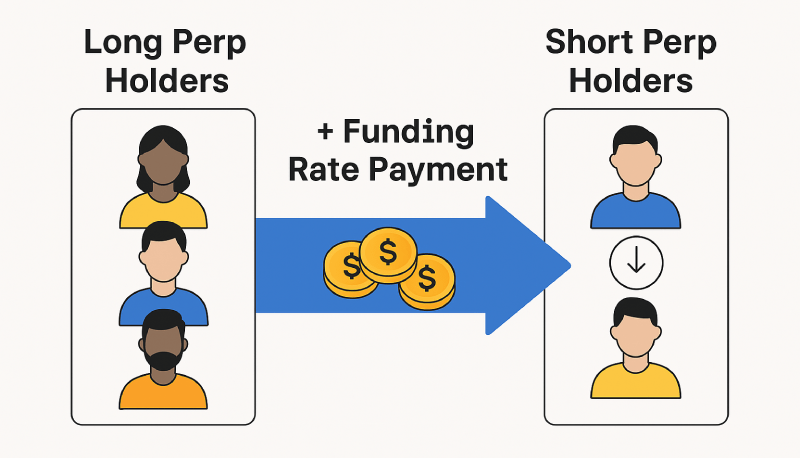

When funding rates are positive, those holding long positions (betting the price will go up) pay those holding short positions (betting the price will go down).

It sounds tempting – just short a perpetual contract and collect payments, right? Well, not quite. If you simply short a perpetual future and the crypto's price skyrockets, your losses on that short position could easily wipe out any funding payments you received.

But what if you could capture those juicy funding payments without exposing yourself to the wild price swings of the crypto market? What if you could structure a trade designed to be largely indifferent to whether Bitcoin moons or dumps?

This isn't magic, but it does require a specific strategy: the basis trade. And the most common flavour, the one we'll dissect today, is the "classic" basis trade: going long spot crypto while simultaneously shorting its perpetual future. It’s not exactly a free lunch – there are costs and risks involved – but executed correctly, it's a foundational strategy for many sophisticated crypto traders looking for market-neutral yield. It requires precision, monitoring, and often, the right tools. Let's break it down.

What Exactly is the Basis Trade (The Classic Version)?

Before diving into the trade setup, let's clarify "basis." In simple terms, basis is the difference between the spot price of an asset and its futures price. If BTC spot is $50,000 and a BTC futures contract trades at $50,100, the basis is +$100.

Now, it's crucial to understand the specific type of futures contract we're usually dealing with in crypto: the perpetual future, often called a 'perp'. Unlike traditional futures contracts in commodities or finance, which have a set expiration date (e.g., the June oil contract expires in June, forcing traders to either close their position or 'roll' it to the next contract month), perpetual futures, as the name suggests, don't expire.

This novel financial instrument was pioneered by Arthur Hayes and his team at the BitMEX exchange around 2016. They faced a challenge: how to create a leveraged derivative product for Bitcoin that behaved like the spot market but without the hassle of physical delivery or forced contract rollovers every month or quarter? Traditional futures weren't ideal for the fast-paced, 24/7 crypto market.

Their solution was the perpetual swap contract. To keep the price of this non-expiring contract tethered closely to the underlying spot index price (a calculated price based on spot prices from major exchanges), they introduced the funding rate mechanism. Instead of converging to the spot price only at expiry (like traditional futures), the funding rate acts as a continuous incentive mechanism, typically applied every 1, 4, or 8 hours depending on the exchange.

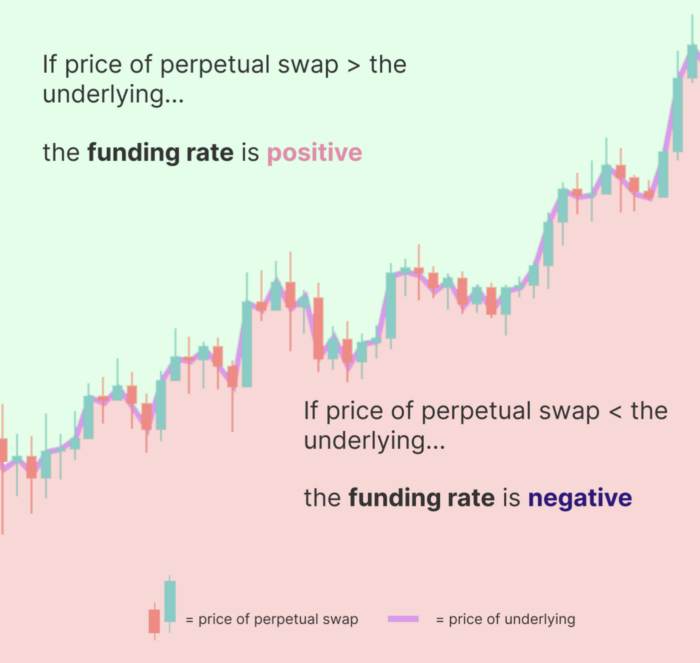

If the perp trades above the spot index (contango), the funding rate becomes positive, and longs pay shorts periodically. This encourages traders to short the perp (selling it) and/or sell spot, helping drive the perp's price down towards the spot index. If the perp trades below the spot index (backwardation), the funding rate becomes negative, and shorts pay longs. This incentivizes traders to long the perp (buying it) and/or buy spot, helping push the perp's price up towards the spot index. This constant push-and-pull, driven by the funding rate, allows the perpetual future to track the spot price remarkably well over time, while still offering high leverage and eliminating the need for expiry dates. It’s this funding rate mechanism that basis traders primarily seek to capitalize on.

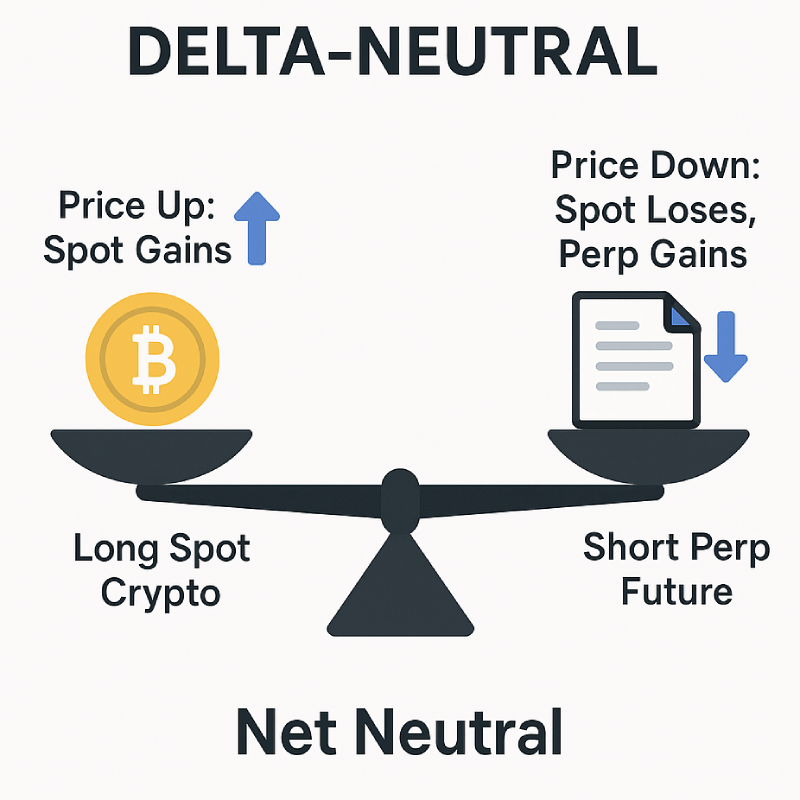

With that understanding, the "classic" basis trade setup involves two simultaneous actions:

- Go Long Spot: You buy and hold the actual cryptocurrency – let's say Bitcoin (BTC) – on an exchange's spot market. You now own BTC.

- Go Short Perp: At the exact same time, you sell (go short) the BTC perpetual future contract for the exact same amount of BTC on the same or a different exchange's derivatives market.

Why do this? The goal is to achieve a state known as delta-neutral. "Delta" is a term borrowed from traditional finance options trading, basically measuring how much a position's value changes when the underlying asset's price changes. Delta-neutral means your overall position's value isn't significantly affected by the ups and downs of the crypto's price.

Think about it:

- If the price of BTC goes up by $100: Your long spot BTC position gains $100 in value. Your short BTC perp position loses roughly $100 in value. The net change is close to zero (ignoring tiny fluctuations in the basis itself).

- If the price of BTC goes down by $100: Your long spot BTC position loses $100 in value. Your short BTC perp position gains roughly $100 in value. Again, the net change is close to zero.

You've effectively hedged out most of the directional price risk. So, if you're not making money from the price going up or down... where does the profit come from?

Distinguishing Basis Trades from Other Delta-Neutral Plays

Now, it's easy to get different delta-neutral strategies mixed up, especially since they often involve perpetual futures and funding rates. Many traders, particularly those newer to these concepts, sometimes confuse the basis trade we're discussing with another popular strategy: the long/short funding rate arbitrage. Let's quickly clarify the difference, as understanding this is key:

- Basis Trade (Classic): Involves one spot position and one perpetual future position on the same underlying asset. You buy the spot asset and simultaneously short the perpetual future. Your primary profit drivers are collecting positive funding rates on the short perp leg and potentially benefiting from the basis (the gap between spot and perp price) narrowing.

- Reverse Basis Trade: This is the mirror image. You short the spot asset (requires borrowing the asset) and simultaneously go long the perpetual future. This is typically done when funding rates are negative (shorts pay longs), allowing you to collect funding on your long perp leg.

- Long/Short Funding Rate Arbitrage: This strategy involves two perpetual future positions on the same underlying asset, but on two different exchanges. You go long the perp on the exchange with the lower funding rate (or more negative/less positive) and simultaneously short the perp on the exchange with the higher funding rate (or less negative/more positive). Your profit comes purely from the difference (the spread) between the two funding rates. You don't hold any spot asset in this trade.

While all these strategies aim for delta-neutrality and often involve funding rates, their structure, execution, profit sources, and risk profiles are distinct. Our focus today is squarely on the classic Basis Trade (Long Spot / Short Perp).

Show Me the Money: How Does the Basis Trade Generate Profit?

If your position is delta-neutral, profiting from price direction is off the table. Instead, the basis trade aims to capture yield from other market dynamics, primarily funding rates.

1. The Primary Driver: Positive Funding Rates

As we discussed, perpetual futures use funding rates to stay anchored to the spot price.

- Positive Funding: When the perp trades at a premium (contango), longs pay shorts.

- Negative Funding: When the perp trades at a discount (backwardation), shorts pay longs.

This funding mechanism essentially balances the demand for leverage between buyers (longs) and sellers (shorts). When more traders want to go long with leverage than short – perhaps because sentiment is bullish – they effectively 'pay' for that privilege via positive funding rates, making it attractive to be on the short side (if hedged). Conversely, if panic selling hits and more traders want to short with leverage, funding can go negative, and shorts pay longs.

In our classic basis trade (Long Spot / Short Perp), you are holding the short position on the perpetual contract. Therefore, when funding rates are positive, you are the one collecting the payments. This is typically the main engine of profit for this strategy.

Let's revisit our simplified example with a bit more context:

- You execute a basis trade on ETH worth $50,000.

- You buy $50,000 worth of ETH on the spot market.

- You simultaneously short $50,000 worth of ETH perpetual futures.

- The funding rate on the exchange where you hold the short perp is +0.01% and is paid every 8 hours. (While our example uses 0.01%, funding rates can fluctuate significantly. They might hover near zero for extended periods, spike to 0.05%, 0.1% or even higher during extreme market euphoria or specific coin hype cycles, or dip negative during sharp sell-offs. Consistent, stable positive rates are the basis trader's bread and butter.)

- Calculation: $50,000 * 0.01% = $5.00

- You collect $5.00 every 8 hours. That's $15.00 per day.

To understand the potential return on your capital, let's annualize this:

- Daily earnings: $15.00

- Annual earnings: $15.00 * 365 = $5,475

- Annual Percentage Rate (APR): ($5,475 / $50,000) * 100% = 10.95% APR

This APR comes just from collecting the funding payments, assuming the rate stays constant (a big assumption, but useful for illustration). You're earning this yield while being largely insulated from whether ETH's price is $2,000 or $4,000.

2. The Secondary Driver: Basis Convergence

There's another potential source of profit, though it's often less predictable or significant than funding. Remember, the basis is the difference between the spot and futures price. While funding helps keep them linked, the basis can still fluctuate based on market sentiment, leverage demand, and liquidity.

If you enter your basis trade when the perp price is significantly higher than the spot price (a wide, positive basis, deep contango), and that gap narrows while your position is open (the basis "converges" towards zero or even goes negative), your short perp position inherently gains value relative to your spot position. When you eventually close both legs simultaneously, this convergence provides an additional boost to your overall profit.

Conversely, if you enter when the basis is narrow and it widens significantly after you enter (perhaps due to a surge in long leverage demand), it could slightly detract from your overall P&L when you close. For most delta-neutral traders focusing on yield farming via funding rates, targeting positive funding is the primary goal, and basis convergence/divergence is often viewed as a secondary factor influencing the final P&L upon exit.

Okay, I Get It. How Do I Do It Manually? (The Hard Way)

Conceptually, the trade seems straightforward enough. Buy low (spot), sell high (perp, relatively speaking via funding), hedge the price risk. Let's walk through the granular steps if you were to execute this manually, highlighting the potential pitfalls:

- Find the Opportunity: This requires constant scanning. You need data feeds or browser tabs open for multiple exchanges (Binance, Bybit, KuCoin, WOO X, OKX, etc.) and potentially dozens of crypto assets (BTC, ETH, SOL, altcoins...). You're looking for assets where the perpetual future consistently shows a positive funding rate and where the current basis (perp price vs. spot price) isn't so wide that it negates the funding yield upon entry. You need to compare rates across exchanges too, as they can differ.

- Calculate Position Size: Decide your capital allocation. Crucially, you need enough capital for the spot purchase and sufficient collateral (margin) deposited in your derivatives/futures wallet for the short perpetual position. Under-margining the short leg is asking for trouble.

- Check Wallet Balances & Transfer Funds: Ensure you have the necessary stablecoins (like USDT or USDC) or base currency in the correct wallets on the chosen exchange(s). You might need funds in your Spot/Funding wallet for the purchase and funds in your Derivatives/Futures wallet for the short collateral. This often involves internal transfers within the exchange.

- Execute Leg 1 (Buy Spot): Navigate to the spot trading interface (e.g., ETH/USDT). Decide on order type: Market order for speed (risks slippage), Limit order for price control (risks partial or no fill). Place your buy order (e.g., buy 10 ETH). Watch the order book and your fills intently. Note the exact quantity filled (e.g., 9.998 ETH due to fees/rounding) and the average execution price.

- Execute Leg 2 (Short Perp): IMMEDIATELY – and we mean within milliseconds if possible – switch tabs or interfaces to the perpetual futures market for the same asset (e.g., ETH/USDT perp). Place a sell/short order for the exact same quantity you just bought on spot (e.g., short 9.998 ETH). Again, choose Market or Limit. Monitor the fill price and ensure the full quantity is executed.

The emphasis on IMMEDIATELY and EXACT SAME QUANTITY cannot be overstated. The entire premise of being delta-neutral relies on entering both legs simultaneously at effectively the same underlying asset price. Any delay allows the market to move, introducing directional risk ('legging risk'). Any size mismatch means you're no longer perfectly hedged.

The Headaches of Manual Basis Trading (Why It's Tougher Than It Looks)

If you've only ever bought spot or maybe dabbled in simple futures trades, attempting a perfect basis trade manually, especially across different exchanges or with significant size, can quickly become a stressful, error-prone ordeal. Here's a deeper look at why:

Finding & Tracking Opportunities: A Constant Chore

Funding rates aren't static billboards; they are dynamic results of market forces. They change every funding period (1h, 4h, 8h) and can fluctuate based on intraday price action and leverage demand. Manually checking dozens of potential pairs across multiple exchanges requires constant vigilance. You might build a watchlist, but then you need to fetch real-time spot prices, perp prices, and the current/predicted funding rate for each, then calculate the potential APR. By the time you identify a seemingly great opportunity, verify the data, and prepare to trade, the rate might have compressed, or the basis might have shifted unfavorably. It's a full-time job just to stay on top of the landscape.

Monitoring the Position: Spreadsheet Hell Intensified

Getting into the trade is only half the battle. Managing it requires meticulous tracking, often relegated to the dreaded spreadsheet. Imagine your spreadsheet growing row by row, position by position: Columns for Entry Date/Time, Asset, Exchange (Spot Leg), Exchange (Perp Leg), Entry Spot Price, Entry Perp Price, Spot Quantity, Perp Quantity, Initial Capital Deployed, Current Spot Price (live feed?), Current Perp Price (live feed?), Spot P&L, Perp P&L (don't forget trading fees!), Last Funding Rate, Funding Received (per period), Timestamp of Last Payment, Total Funding Received To Date, Net P&L (Spot + Perp + Funding - Fees), Current Margin Ratio (%), Perp Liquidation Price...Now multiply this complexity by 5, 10, or 15 simultaneous positions across maybe 3-5 different exchanges. The constant need for data entry (or complex API scripting if you have the skills), formula checking, reconciling data across various exchange UIs and reports... it induces a unique kind of mental fatigue. It's incredibly prone to copy-paste errors, missed updates during volatile periods, or miscalculations, especially when trying to get a real-time overview of your entire portfolio's risk and return. This isn't just "not fun," it's actively detrimental to effective risk management and timely decision-making.

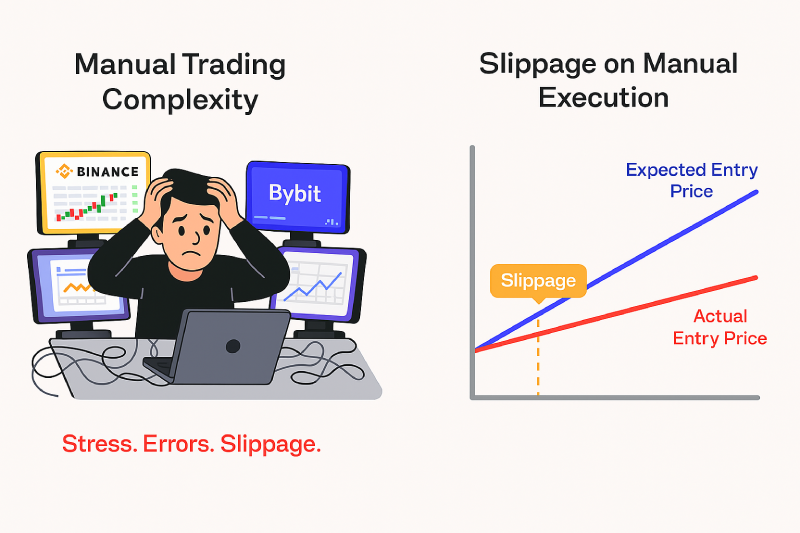

Execution Risk & Slippage: The Silent Killer

Crypto markets are notoriously volatile and operate 24/7. Prices can whip around in seconds. The tiny delay between your spot buy fill and your perp short entry – even if it's just 5-10 seconds of navigating interfaces and clicking – can see prices move significantly.

This "slippage" – the difference between the price you expected based on your analysis and the price you actually got filled at – directly attacks your potential profit margin, which is often thin to begin with (the basis or the funding rate).Using market orders seems like the solution for speed, but you're at the mercy of the current order book depth. In volatile moments or on less liquid pairs, your market order could fill at drastically worse prices than anticipated ('blown through' the book). Using limit orders gives price certainty if they fill, but you risk only one leg executing, leaving you exposed (e.g., your spot buy fills, but the price ticks up before your perp short limit order is hit). This failed execution leaves you with an unintended long position, not the delta-neutral setup you wanted.

Remember that ~11% APR example on $50k? Let's say combined slippage across both legs costs you just 0.15% of the position value on entry. That's 75 gone instantly (50,000 * 0,15%). If the expected daily funding profit was only $15, that's five full days worth of potential earnings vaporized simply due to execution friction. This makes capturing small, consistent edges via manual execution incredibly challenging and often demoralizing.

Enter BTX: Basis Trading Made Efficient and Accessible

Doing basis trades precisely, efficiently, and at scale manually is, frankly, a massive operational headache prone to costly errors. It requires speed, accuracy, and constant vigilance that few individual traders can sustain without significant time investment or custom tooling.

This is exactly why we built the Basis Trade eXecutor (BTX).

Important Note: How BTX Connects (It's Not Magic)

Before we dive into how BTX streamlines things, let's address a common point of confusion. Some users initially wonder if BTX is a kind of self-contained system or a separate exchange where these trades happen internally. That's not quite right!

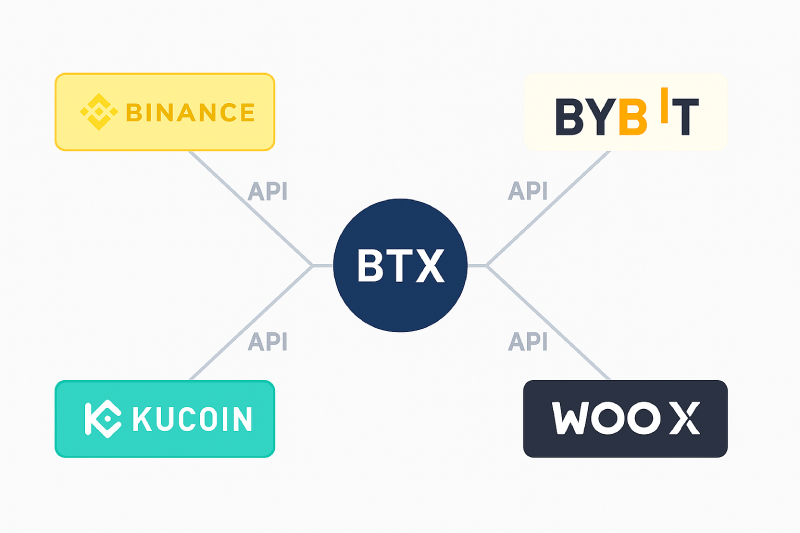

BTX acts as an intelligent execution and monitoring layer on top of your existing exchange accounts. Think of it as a sophisticated remote control for your trading on platforms like Binance, Bybit, KuCoin, WOO X, etc. To use BTX, you first need to:

- Have accounts on the supported exchanges you wish to trade on.

- Generate API keys within those exchange accounts. (These keys grant BTX permission to execute trades and read balance/position data on your behalf – crucially, enable trading permissions but typically disable withdrawal permissions for security).

- Securely add these API keys to your BTX account.

Once connected, BTX uses these keys to place orders, monitor positions, and display information from your linked exchanges directly within the BTX dashboard. You still need accounts, funds, and margin on the underlying exchanges; BTX simply automates the complex actions within those accounts.

Now, let's see how BTX leverages this connection to tackle the manual trading headaches:

- It precisely calculates the required quantities for both the long spot and short perp legs based on your desired capital allocation.

- It sends the orders for both legs simultaneously (or as close to simultaneously as physically possible) to the relevant exchange(s).

- It employs optimized order placement strategies. The principle involves coordinating order placement with microsecond precision, potentially breaking down larger orders into smaller, intelligently timed chunks to minimize market impact and navigate the order book effectively. The goal is to achieve the best possible average fill price for both legs, minimizing costly slippage and preserving the basis you aimed to capture. BTX also handles nuances like varying minimum order sizes, tick sizes (price increments), and quantity precisions across different exchanges and trading pairs, ensuring your desired position size is executed correctly without manual calculation errors.

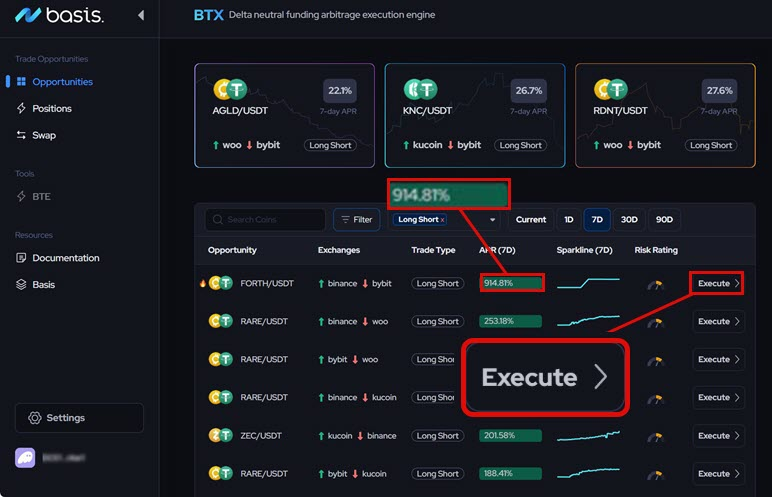

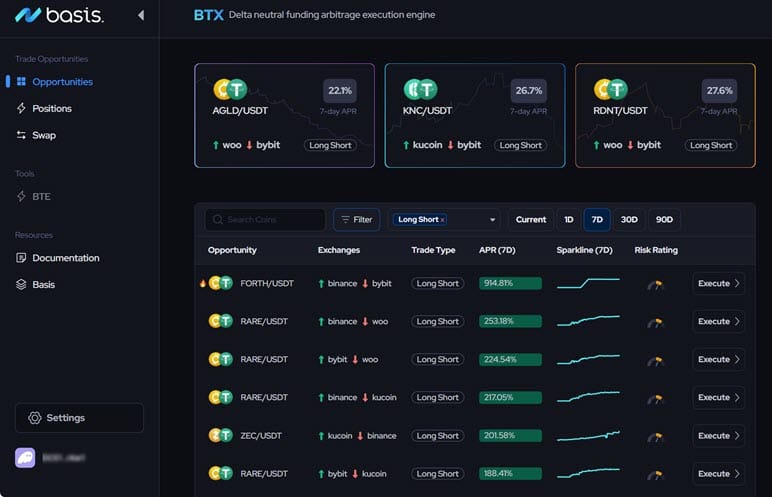

Simplifying Opportunity Discovery

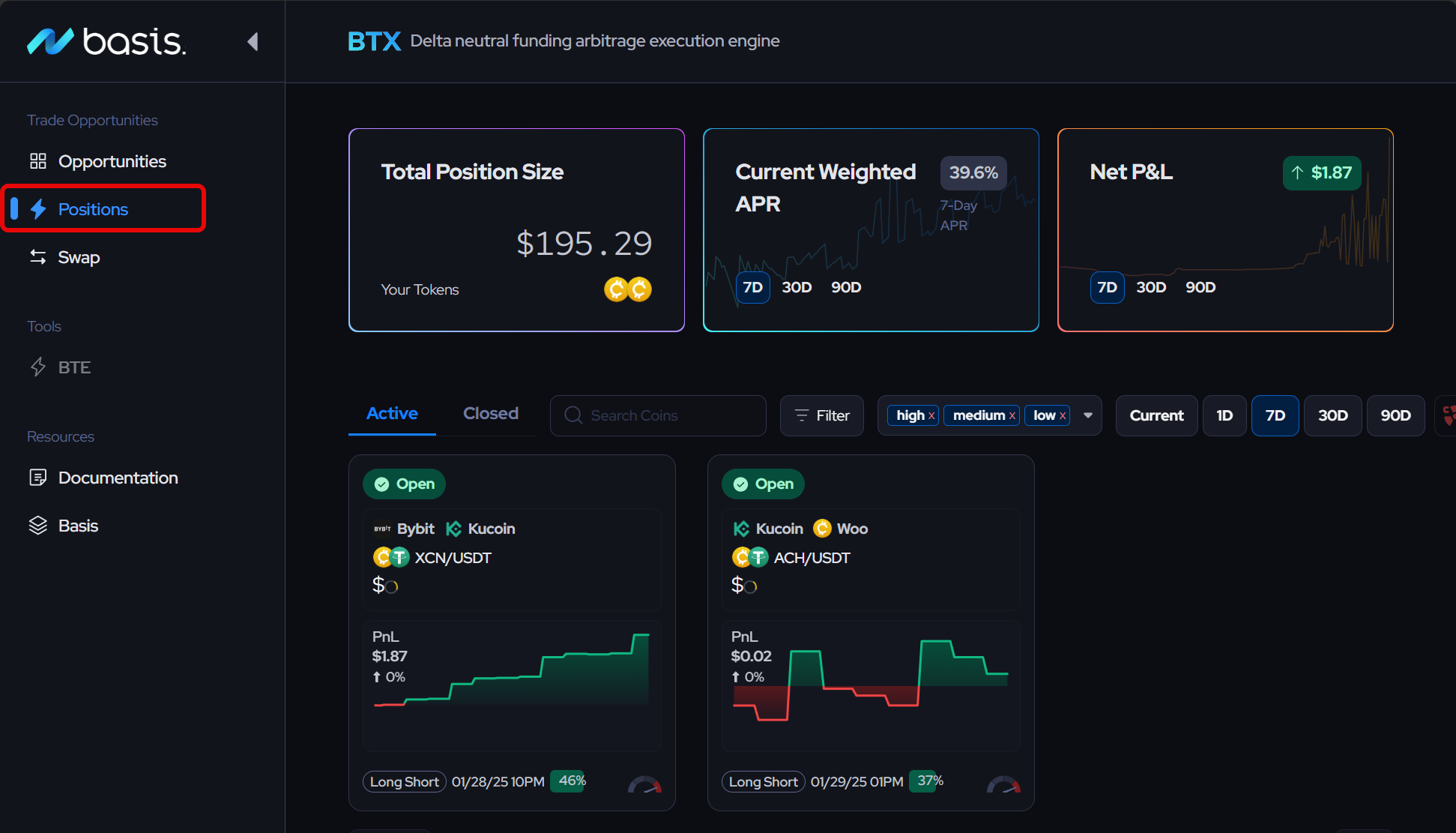

Stop the manual hunt. The BTX interface aggregates and displays potential basis trade opportunities across the supported exchanges and assets it monitors. You can easily view assets, the relevant exchanges, and importantly, estimated APRs based on current funding rates and market prices, helping you quickly identify and evaluate promising candidates without needing to collate data from multiple disparate sources yourself.

- See your overall portfolio P&L and drill down into the performance of each individual basis trade (or Long/Short, Reverse Basis trade).

- Track accumulated funding payments clearly – know exactly how much yield your positions are generating.

- Monitor key risk metrics in real-time, including warnings related to the margin health of your perpetual futures legs. This allows you to proactively manage liquidation risk by adding collateral if needed.

- Manage your positions: Decide to increase or decrease the size of an existing trade (BTX handles the complex task of executing the additional spot/perp orders proportionally and optimally). Or, close out a position entirely with a single command – BTX ensures both the spot and perp legs are closed simultaneously to lock in the P&L and minimize exit slippage.

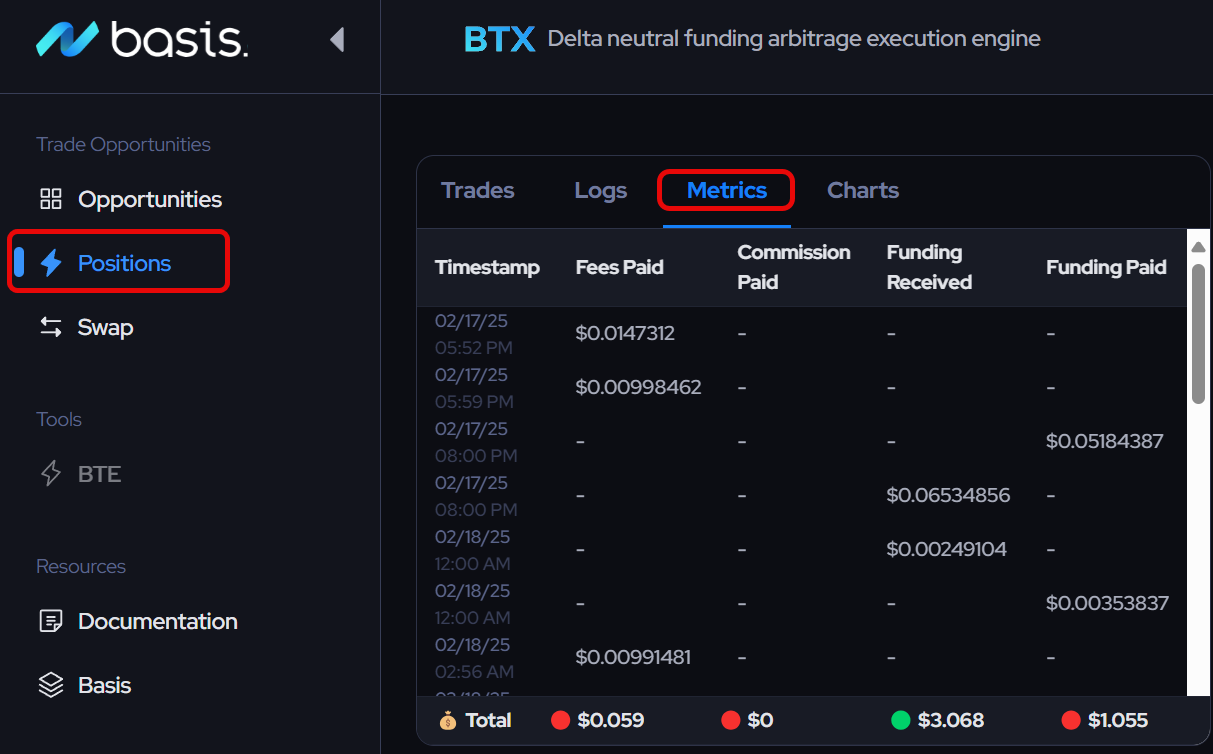

Centralized Monitoring: Your Delta-Neutral Command Center

Obliterate the spreadsheet chaos. The BTX dashboard provides a clean, unified view of all your delta-neutral positions initiated through the platform: this potent combination of automation and clarity makes sophisticated strategies genuinely accessible, even for traders who are new to futures or lack the time to manage complex positions manually. As another user, initially only comfortable with spot trading, shared:

"GM. Been in a SEND Long/Short across ByBit and Woo for 12 days and at 156% APR. It bloody works you know [...] Also, I'm a total newbie to futures trading. Only ever done spot. Without BTX this would be impossible for me. With BTX it's easy."

"With BTX it's easy"

— basis.markets (@basismarkets) January 17, 2025

One of our discord members and BTX users has been at it for 12 days for 156% APR. pic.twitter.com/IhOeMwyr7Z

Solving Execution: Minimizing Slippage is Paramount

This is BTX's foundational value proposition. Instead of you frantically clicking between browser tabs and exchange interfaces, BTX leverages its direct API connections.

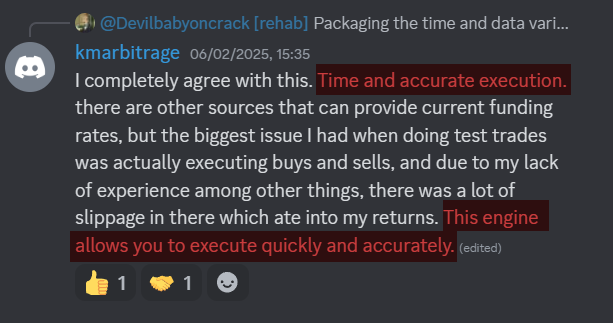

When you decide to execute a basis trade through the BTX interface: this automated, near-instantaneous, and optimized execution is critical for consistently capturing the often-narrow edge offered by basis trades. As one user highlighted, the difference is night and day:

"Time and accurate execution [are important]... There are other sources that can provide current funding rates, but the biggest issue I had when doing test trades was actually executing buys and sells, and due to my lack of experience among other things, there was a lot of slippage in there which ate into my returns. This engine [BTX] allows you to execute quickly and accurately."

Important Considerations & Nuances

While BTX dramatically simplifies execution and monitoring, transforming the operational aspect of basis trading, it's crucial to remember that it's a tool, not a magic money printer. Understanding the underlying mechanics and remaining considerations is vital:

Costs: Every trade incurs fees. Basis trading inherently involves fees on both the spot buy and the perp short (and again when closing both legs). These exchange fees directly reduce your net realized APR. BTX aims to provide visibility into potential APR after estimated fees, but always be cognizant of the specific fee structures on the exchanges you use.

Margin Management: This cannot be stressed enough. You are ultimately responsible for ensuring sufficient collateral is available in your derivatives wallet to withstand adverse price movements. Even though your overall position is delta-neutral, a sharp rally in the crypto's price will cause unrealized losses on the short perp leg, increasing margin usage. Failure to maintain adequate margin will lead to liquidation by the exchange. BTX helps you monitor, but you need to act.

Market Conditions & Strategy Suitability: Classic basis trades (Long Spot / Short Perp) are most profitable when funding rates are consistently positive and reasonably stable. This environment is more common during bull markets or periods of strong speculative interest where demand for long leverage is high. In sharp downturns or periods of market panic, funding can swiftly flip negative, rendering this specific structure unprofitable (though Reverse Basis trades – short spot, long perp – which BTX also supports, might become attractive yield opportunities in such conditions). Choose the right strategy for the prevailing market regime.

Existing risks

BTX powerfully mitigates execution risk and simplifies monitoring. However, other risks inherent to trading and the crypto market still exist and need to be mentioned.

Liquidation Risk: Directly tied to margin management. Always maintain healthy buffers.

Funding Rate Risk: The primary profit driver can disappear or reverse. Funding rates can change rapidly based on market dynamics, impacting your ongoing profitability. A +20% APR trade today could be +5% tomorrow or even negative next week. Continuous monitoring (simplified by BTX) is essential.

Counterparty Risk: You are still exposed to the risks associated with the exchanges you use. This isn't just about the nightmare scenario of an exchange collapsing (like FTX). It also includes more mundane but impactful operational risks: exchanges unexpectedly halting withdrawals during market stress, API systems becoming unresponsive or rate-limited during peak volatility (potentially hindering BTX's ability to manage positions instantly), sudden, poorly communicated changes to margin requirements or leverage limits, or even the abrupt delisting of assets or perpetual contracts you are actively trading. Diversifying capital across multiple reputable exchanges (which BTX facilitates) can help mitigate concentration risk, but doesn't eliminate counterparty risk entirely.

Basis Risk: The difference between spot and perp prices can fluctuate unpredictably, potentially impacting your P&L upon closing the position, independent of the funding collected.

BTX provides the sophisticated tools for superior execution and unified monitoring; robust risk management practices, careful strategy selection based on market conditions, and responsible capital allocation remain squarely in the trader's domain.

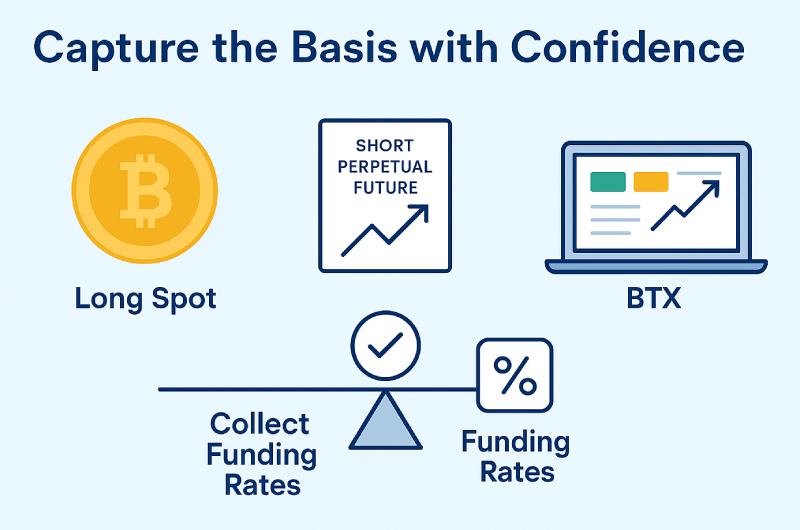

Conclusion: Capture the Basis with Confidence

The classic basis trade – going long spot crypto while simultaneously shorting its perpetual future – is a legitimate and widely used strategy by crypto traders, from individuals to large quantitative funds. It offers a methodical way to generate yield from market structure, primarily by collecting positive funding rates, while significantly reducing exposure to the asset's directional price movements.

However, the theoretical simplicity masks significant practical challenges. Manual execution is notoriously difficult, constantly threatened by slippage that erodes potential profits before they're even earned. Manually identifying opportunities across a fragmented landscape and meticulously monitoring multiple complex positions across different exchanges is inefficient, time-consuming, and prone to costly human error. And as we've discussed, it's crucial to distinguish this spot-vs-perp strategy from other delta-neutral plays like perp-vs-perp funding arbitrage.

This is precisely where automation delivers a powerful, almost essential, advantage. The Basis Trade eXecutor (BTX) allows you to work securely with your existing exchange accounts via API keys, and is purpose-built to tackle these critical, high-friction tasks. It automates the simultaneous execution of both trade legs with algorithms designed to minimize slippage. It provides a clear, centralized dashboard for tracking P&L, monitoring accumulated funding, and managing risk across all your delta-neutral positions. BTX transforms basis trading from a demanding, high-touch manual process into an efficient, scalable, and more accessible strategy.

If you're intrigued by the potential of earning yield from crypto market inefficiencies like funding rates, but wary of the volatility of directional bets, understanding the basis trade is a crucial first step. And if you want to implement this strategy effectively, consistently, and without being chained to your trading screen manually managing every intricate detail, leveraging a specialized tool like BTX might just be the decisive edge you need.

FAQ: Your Burning Questions About Basis Trading Answered

Q1: Do I need to be an expert in derivatives to execute basis trades?

Not at all. A basic understanding of spot markets and perpetual futures is enough to grasp the concept. Tools like BTX are designed to simplify the process so that even those new to derivatives can participate effectively.

Q2: Is basis trading truly risk-free?

While basis trading significantly reduces directional risk by neutralizing exposure to price movements, it is not without risk. Funding rates can fluctuate, execution timing can be critical, and fees may impact overall profitability. Proper risk management is essential.

Q3: How long should I typically hold a basis trade?

There is no one-size-fits-all answer. The optimal holding period depends on market conditions, the size of the basis, and the stability of funding rates. Some trades may last a few hours, while others could extend over several days or weeks. The key is to monitor the spread and exit when the opportunity diminishes.

Q4: Do I need to have accounts on multiple exchanges to execute a basis trade?

Yes, because basis trading inherently involves both spot and perpetual markets, which are often hosted on different exchanges. While BTX automates the process via API integration, you still need active accounts on the relevant platforms.

Q5: What happens if the funding rate flips unexpectedly?

Funding rate flips are one of the primary risks in basis trading. If the funding rate reverses, it can reduce or even negate your expected profits. Automated systems like BTX help mitigate this risk by continuously monitoring market conditions and rebalancing trades as needed.

Q6: How does the pricing gap eventually converge?

The convergence of the spot and perpetual prices is driven by market forces and the periodic funding rate mechanism. As funding rates incentivize traders to correct mispricings, the spread between the two markets tends to narrow over time. This is when the basis trade realizes its profit.

Ready to explore basis trading without the manual headaches and execution risks?

- Check out the real-time basis trade opportunities currently listed within the BTX platform. You need a Basis NFT, get one here.

- Join our Discord community to connect with fellow delta-neutral traders and the BTX team.