Position Sizing & Capital Allocation for Delta-Neutral Strategies

Learn how to size trades and allocate capital in delta-neutral strategies. A guide to risk, discipline, and building sustainable crypto yield.

(How to Size Trades and Build a Sustainable Yield Portfolio with BTX)

1. Introduction: Why Capital Management Matters

Most traders in crypto fixate on the wrong thing.

They chase screenshots of triple-digit APRs, hop from token farm to token farm, and dream of “the trade” that changes their net worth in one move. But that’s not how wealth is built. Not sustainably.

The traders who survive and actually grow their stack, understand something deeper: capital management is the strategy.

Even the most bulletproof delta-neutral trade can be destroyed if you size it recklessly. Conversely, even a modest opportunity can compound meaningfully if you allocate with discipline.

Think about it like driving a car. BTX is the engine. But the engine alone doesn’t keep you alive. How much throttle you apply, how you brake, and how you steer the capital you deploy: that’s what keeps you on the road.

This guide is about exactly that: how to size and allocate your capital responsibly when running delta-neutral strategies.

By the end, you’ll have a framework for:

- How to separate your “degen” bets from your income engine.

- How much to allocate to delta-neutral at the portfolio level.

- How to size individual positions intelligently.

- How to manage exposure across multiple trades.

- How to scale up or down dynamically without emotional decision-making.

And you’ll see how BTX gives you the tools to make this discipline real, not just theory.

2. The “Two Portfolios” Mindset

One of the biggest mistakes traders make is trying to lump everything into one pool of capital. They throw their entire net worth at whatever looks shiny this week — a meme coin pump, a basis trade, a staking yield farm.

That’s a recipe for chaos.

Instead, think in terms of two portfolios:

- Directional / Speculative Stack

- This is where you place bets on market direction.

- It’s your “degen” stack: spot positions, swing trades, leveraged punts, NFTs, memecoins.

- You accept volatility here. You accept drawdowns. It’s your speculative sandbox.

- Delta-Neutral / Yield Stack

- This is the engine of consistency.

- These are your basis trades, reverse basis, long/short arbs.

- The goal is not to 10x in a week. The goal is compounded, low-volatility yield.

- This stack is about stability, not adrenaline.

By mentally separating these, you avoid the fatal error of treating BTX strategies like speculative moonshots. You respect them for what they are: yield engines that demand discipline.

3. How Much Capital to Allocate to Delta-Neutral Strategies?

Allocation is not a moral question (“am I brave enough?”). It’s a systems question: What percentage lets you learn, compound, and survive errors—without dulling your edge or inviting ruin? The ranges below aren’t commandments; they’re lanes, and each lane has trade-offs.

Beginner / Conservative (5–10% of total net worth).

At this stage, the prime objective isn’t yield, it’s familiarity under live fire—seeing funding flip in real time, watching margin breathe through volatility, using BTX’s Increase/Decrease without panic. Five to ten percent is the band where a mistake stings but doesn’t scar. Psychologically, this is crucial: if you oversize out of the gate, every candle becomes an adrenaline event and you will either churn (overreact) or freeze (under-react). A smaller allocation gives you emotional bandwidth to observe, journal, and iterate a process. The obvious trade-off: you won’t post heroic P&L screenshots. That’s fine. You’re building a cockpit, not chasing a dopamine hit.

Intermediate / Moderate (15–25%).

You understand the mechanics, can read funding history, and know your personal freak-out threshold. Here, the returns become meaningful without the portfolio becoming hostage to a single venue or strategy. The psychological edge is confidence with a governor: big enough to care, small enough to think clearly. The trade-off: discipline gets tested. At ~20% allocation, opportunities start to “call your name.” You’ll feel the pull to add “just one more” position—often where slippage and concentration risk sneak in. This is where pre-committed caps (per exchange, per strategy) save you.

Advanced / Aggressive (30–40%).

Delta-neutral becomes a core income engine. You’ve likely diversified venues, keep dry powder, and treat sizing as a living parameter—responsive to volatility regimes. The psychological challenge flips: complacency. Because neutral yield feels “safe,” it’s tempting to drift higher. Resist it. The incremental utility of moving from 40% to 60% is rarely worth the tail-risk you add.

Why not “go all in” on CEX-based neutral? Counterparty risk.

Delta-neutral compresses market risk; it does not erase venue risk. Centralized exchanges can halt withdrawals, change margin policies, throttle APIs at the worst moment, or—rarely but catastrophically—fail. Even absent blowups, operational friction (maintenance, partial outages) is a real drag. This is why seasoned traders spread exposure: caps per exchange (e.g., no more than 25–35% of the delta-neutral stack on a single venue), caps per strategy type (e.g., no more than 40% in any one strategy family), and a standing cash buffer for margin top-ups or opportunistic adds. The point is simple: diversify the pipes that feed your engine. Neutral trades can survive volatility; they can’t survive a shut door.

Bottom line: start where your brain stays calm, scale where your process stays consistent, and never treat CEXs as riskless utilities. Allocation is the most durable edge you control.

4. Sizing Individual Positions

Once you’ve decided how much of the portfolio goes to delta-neutral, the next question is how big any given trade should be. Three models dominate. Each can be “right” depending on your stage and the market regime.

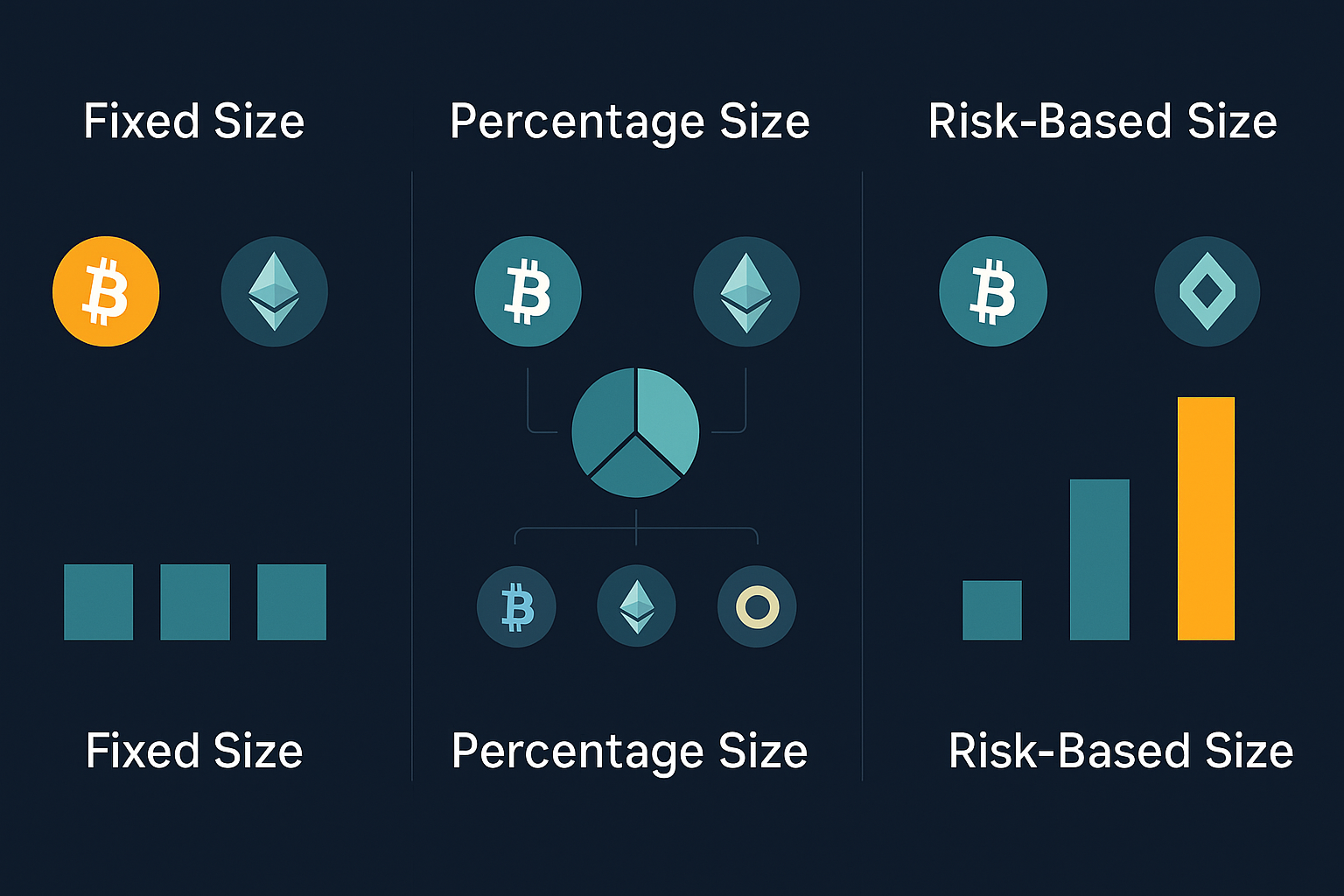

Model A — Fixed Size Allocation

What it is: Every trade gets the same dollar size (e.g., $1,000 each).

Why it works: It’s cognitively frictionless. You don’t burn decision energy calibrating size; you spend it on selection and timing. For new users, that simplicity keeps emotions in check.

Narrative: With a $10,000 delta-neutral stack, you might fix at $500 per trade. You’ll quickly learn the full cycle—open, monitor, close—without the “did I oversize this alt trade?” anxiety. The cost of simplicity is bluntness: you’ll under-weight high-quality opportunities (BTC basis in a stable regime) and over-weight jumpy ones (thin alt L/S during a news week). That’s acceptable while you’re building muscle memory, but as your eye improves, you’ll want finer tools.

When to graduate: When you find yourself consistently thinking “This BTC basis deserves more” or “This alt pair should be a toe-dip,” you’re ready for the next model.

Model B — Percentage of Portfolio

What it is: Each trade is a fixed % of the delta-neutral stack (e.g., 5–10%).

Why it works: It scales naturally with your account and implicitly caps concurrency.

Walkthrough: You have a $10,000 delta-neutral stack.

- At 5% per trade, each position is $500.

- Four concurrent trades = 20% deployed; ten trades = 50%.

- If you lift your per-trade size to 8%, you’re implicitly capping yourself at ~6 concurrent trades before hitting 50% deployment.

Narrative: The percentage model is a great middle path. You’re no longer treating all trades as equal, because you can lift or lower the base % in different regimes (e.g., 5% during high-vol weeks; 8% when books are deep and funding is calm). But like the fixed model, it’s still coarse: a volatile alt opportunity can still accidentally earn the same size as a serene BTC basis unless you intervene.

When to graduate: When you catch yourself routinely overriding the percentage for specific trades, you’re doing risk-based sizing by instinct. Make it explicit.

Model C — Risk-Based Sizing (Pro Level)

What it is: Size proportionally to the risk/quality of the opportunity: volatility, liquidity, funding stability, and operational complexity.

Detailed Scenario:

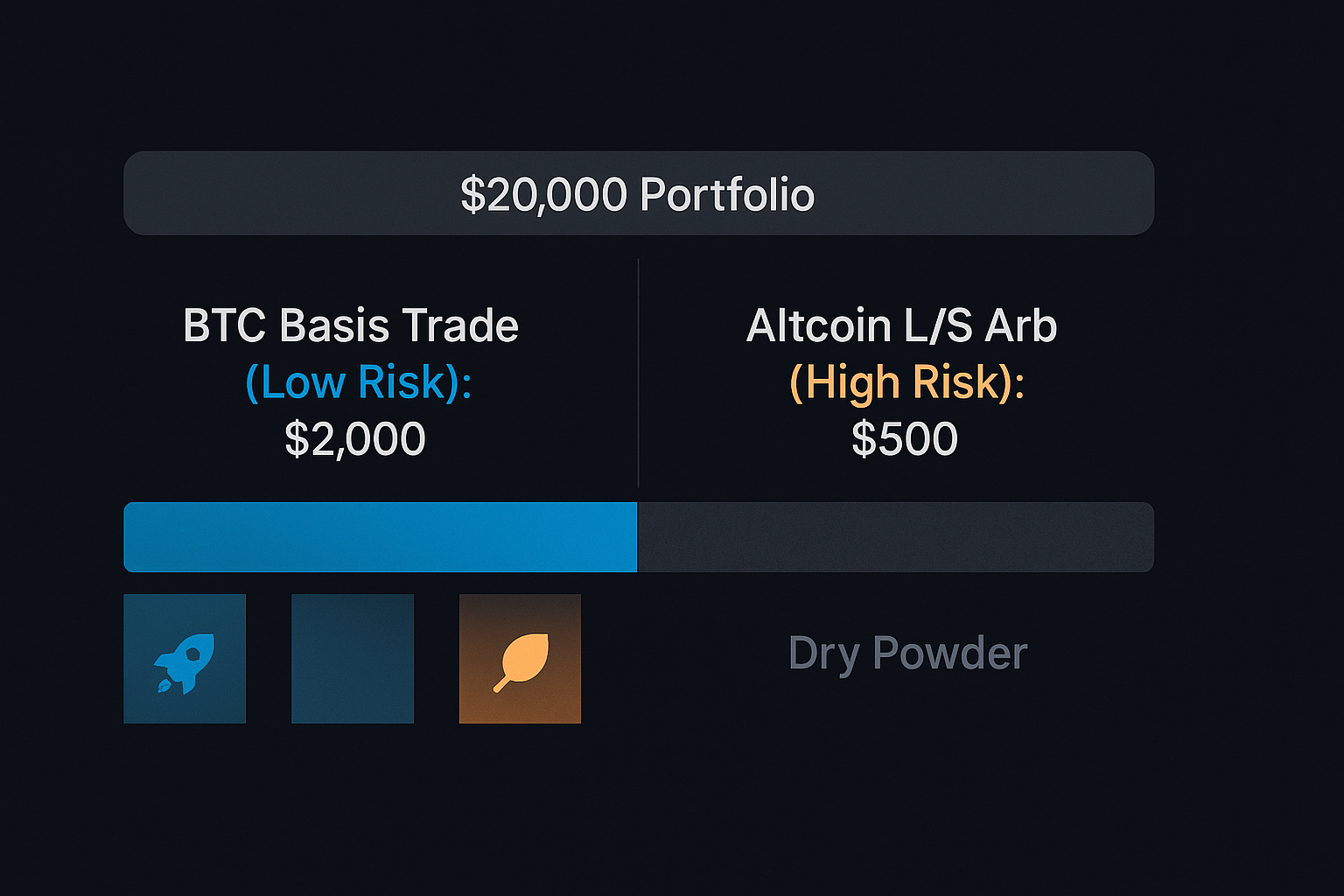

Trader A has a $20,000 delta-neutral stack. Two opportunities appear on BTX:

BTC Basis Trade — 2-15% APR, deep liquidity, funding history flat and positive for weeks, tight spreads, low operational complexity.

New Alt L/S Arb — 150% APR headline, but funding has flipped 3 times this week, books are thin, spread widens during US lunch hours, borrow fee spikes on news.

Thought process:

- Liquidity & Slippage: BTC fills clean even at size; the alt pair pushes price and suffers spread expansion.

- Funding Stability: BTC shows orderly mean-reversion; the alt is noisy and reflexive (high APR because the crowd just discovered it).

- Operational Complexity: BTC basis = straightforward. Alt L/S = more monitoring, more scope for error.

- Tail Risk: If the alt funding snaps negative while borrow fees jump, your “150%” can turn into a drip or a drain.

Sizing decision:

- Allocate 10–12.5% to BTC basis ($2,000–$2,500).

- Allocate 2–3% to the alt arb ($400–$600).

- Keep dry powder (~5–10%) for either topping up margin on a wobble or adding to BTC if conditions keep improving.

Why more to the lower APR? Because risk-adjusted return matters. A steady 15% that you can hold and pyramid beats a flashy 150% that vanishes on a funding flip. Capacity matters too: you can scale BTC without moving the market; you can’t scale the alt without chasing your own fills.

Operational plan (with BTX):

- Open BTC basis at $2,000. Monitor the Risk Velocimeter (green) and live margin. If stable for 3–5 days, Increase by $500–$1,000.

- Open the alt at $500. Set personal triggers: if funding variance exceeds your tolerance or spreads widen beyond X bps, Decrease to $250 or close.

- Review both daily: if BTC stays serene, pyramid again; if the alt behaves, consider a tiny add, but never let it eclipse 3–4% of the stack.

Result: You’ve honored the siren song of high APR with a measured toe-dip while letting the quiet compounding machine (BTC basis) carry the weight. That’s risk-based sizing in practice: pay the market for certainty, and charge a premium for chaos.

5. Managing Total Exposure

Individual trades can look tidy while the portfolio quietly drifts into danger. This is “style drift” in delta-neutral: you start with a clean plan (a few small, uncorrelated positions) and end up with a cluttered book... too many trades on one venue, too much in one strategy family, too little dry powder to maneuver.

Expanded scenario:

You’re running a $10,000 delta-neutral stack with a 5% per-trade base size ($500). Week one, you open four positions (20% deployed). Feels conservative. Mid-week you add two more because APRs pop (now 30%). Friday brings another “can’t-miss” setup and... because everything is green, you add three small alts at $300 each. You’ve drifted to ~39% deployed, 60% of it on one exchange, and half of it in the same strategy family. Nothing looks scary in isolation, but the aggregate risk is now path-dependent: one venue outage, one policy change, and you’re effectively frozen.

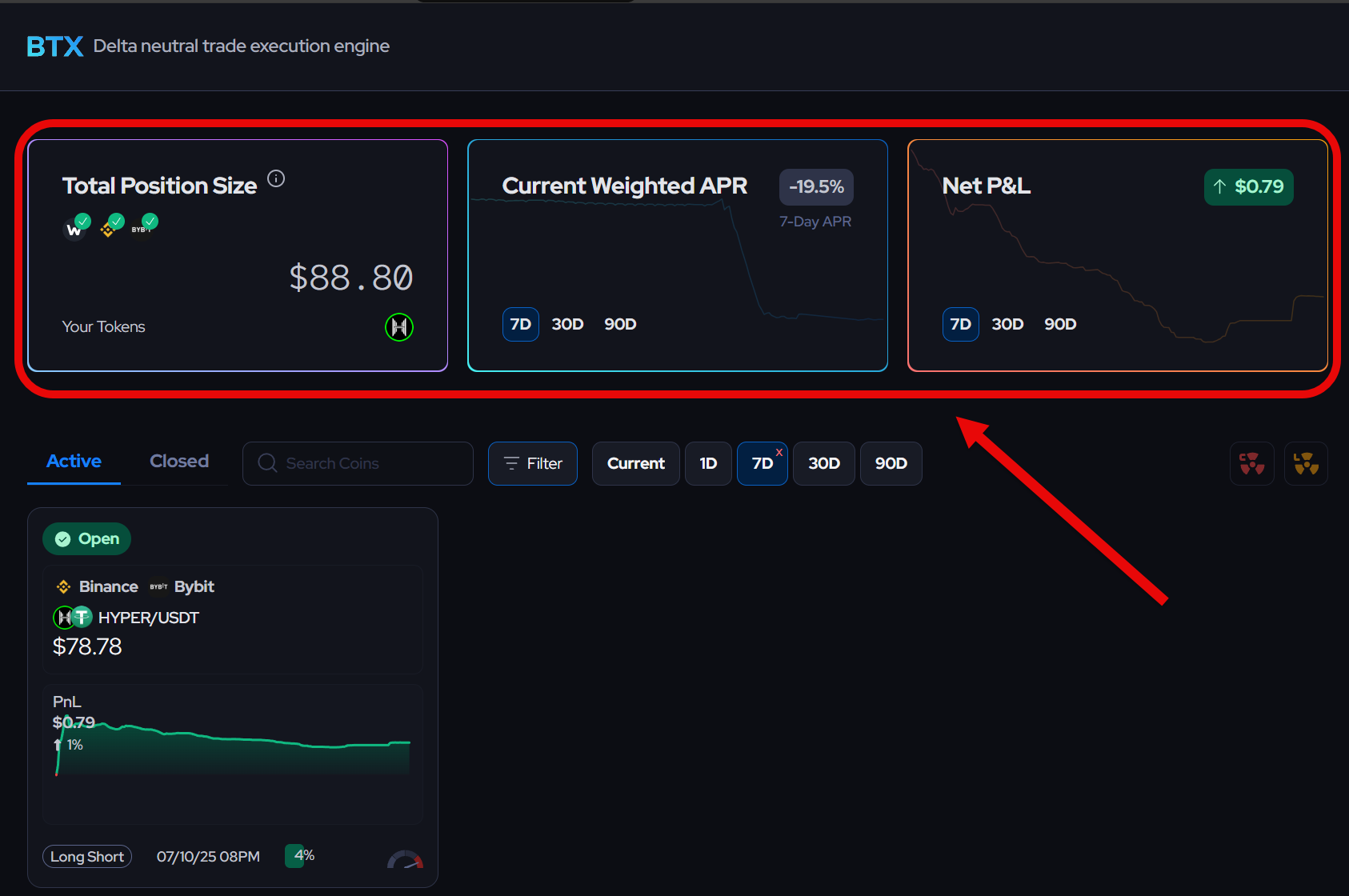

How to use the BTX dashboard as a routine check:

- Daily glance (2–3 minutes):

- Total Exposure % (How much of the stack is deployed?)

- Exposure by Exchange (Any venue over 25–35%?)

- Exposure by Strategy Family (Basis vs. Reverse Basis vs. L/S)

- Risk Velocimeter per position (Are any drifting yellow/red?)

- Funding Logs (Variance creeping up?)

- Weekly review (10–15 minutes):

- Concentration caps: if an exchange > 35%, trim or migrate one position.

- Strategy balance: if one family > 40%, seek diversification or reduce weakest link.

- Dry powder: maintain 10–20% cash for top-ups/opportunities.

- Action list: identify one Increase (proven, green) and one Decrease (noisy, widening spreads).

Practical rule of thumb:

- If Total Exposure > 50%, new trades must be exceptional or offset by reductions elsewhere.

- If two metrics flash at once (e.g., venue concentration + rising funding variance), take a portfolio action, not a trade-by-trade tweak.

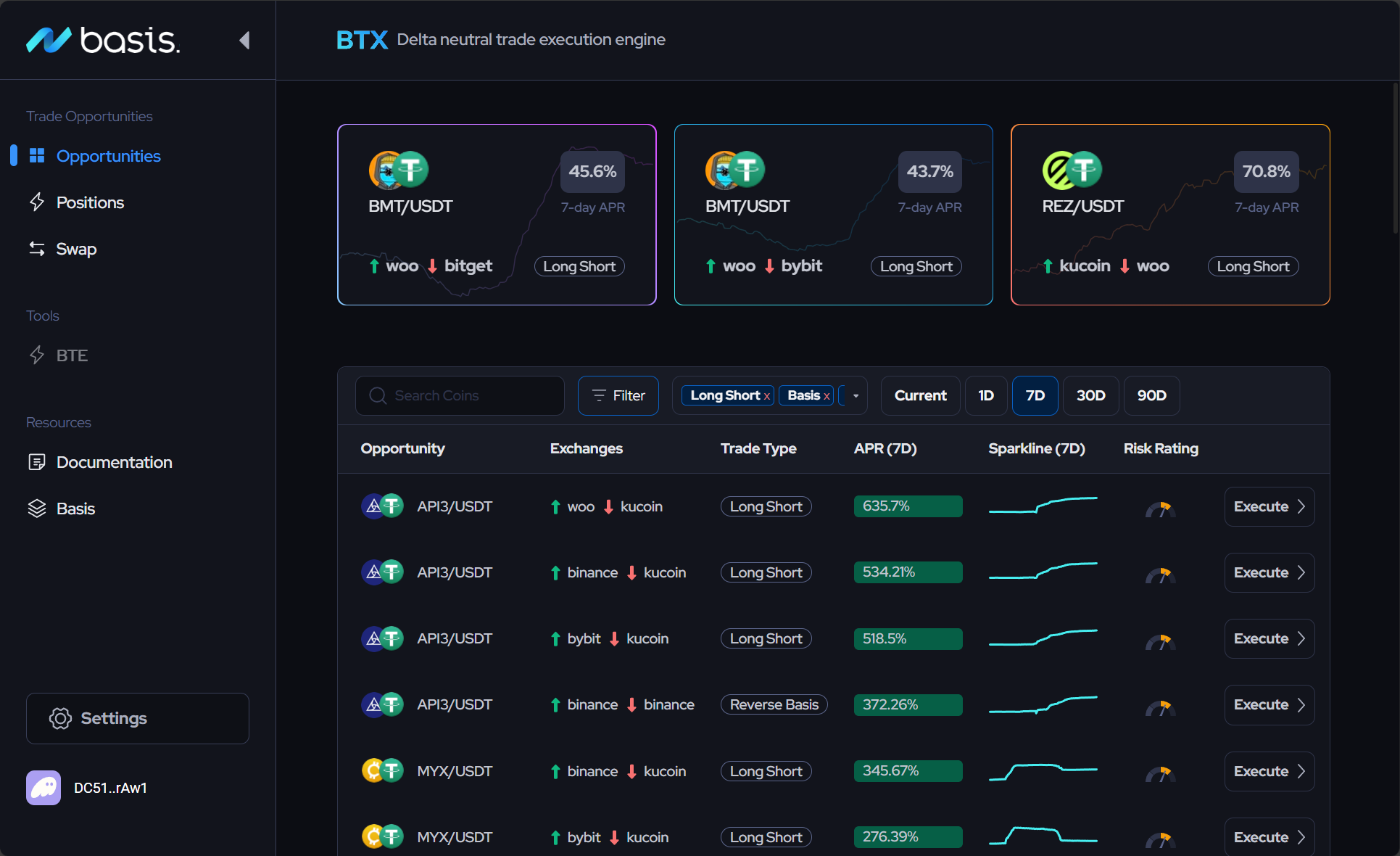

The discipline is simple: see the forest every day, prune the branches every week. BTX gives you the forest: Total Exposure, venue breakdowns, unified APR/P&L, so style drift doesn’t sneak up while you’re busy celebrating individual winners.

6. Pyramiding & Scaling Strategies

Smart traders don’t just set positions and forget them. They scale dynamically.

Scenario:

- You open a $500 BTC basis trade.

- After 7 days, APR is steady at 18%, margin health is strong, funding hasn’t flipped.

- Instead of chasing a new trade, you Increase the size by another $250.

Now you’ve pyramided into a stronger allocation where the odds are proven.

On the flip side:

- You open a $500 altcoin L/S arb.

- Funding is erratic, APR swings negative overnight.

- You Decrease size to $250, protecting capital.

This is the kind of proactive risk control pros use... but without BTX, it requires multiple manual orders and high slippage risk. With BTX, scaling is one click.

7. Psychological Edge: Discipline Through Sizing

Sizing isn’t just math. It’s psychology.

- Oversize a trade → you panic at the first sign of red.

- Undersize a trade → you get bored, overtrade, or chase yield elsewhere.

Good sizing = emotional neutrality.

You let the strategy work because you’ve already controlled the downside.

This is the invisible edge. Most traders blow up not because their strategy was wrong, but because their sizing was wrong.

Delta-neutral isn’t about adrenaline. It’s about consistency. Proper sizing transforms it from “high-stress gamble” to “systematic yield engine.”

8. Conclusion: Capital Management is Risk Management

Every trader wants better yield. Few want to do the boring work of capital management. But the boring work is the difference between those who last and those who disappear.

Remember:

- Separate speculative from yield capital.

- Size positions intelligently.

- Monitor total exposure.

- Scale dynamically.

- Respect your psychology.

BTX is the engine that executes delta-neutral strategies.

But sizing and allocation? That’s the steering wheel. That’s you.

Start small. Trade smart. Build discipline. And watch your yield engine scale.