Macro & Market Review: Market Review, Solana Spotlight & DAO Updates

It's that time again - welcome to the latest Macro & Market Snapshot from Basis Markets.

Halfway through 2024, it's already been an eventful year for economic and crypto markets markets, with the Magnificent Seven marching on, Bitcoin having reached all time highs (at least in nominal terms), the approval of an Ethereum ETF, Solana DeFi peaking, and plenty of new opportunities presenting themselves.

Development progress has continued against the roadmap, with the BTX now at version 0.7.0-beta and incorporating an ever-increasing feature set and list of exchange integrations. The user interface redesign is also well underway, as you may have seen from the sneak peeks shared in the Basis Markets Discord and X, ahead of a BTX public release and launch of BTE 2.0.

These snapshots are designed to give an insight into the global forces shaping the world of macro, markets, futures and flows right now, as well as a deep-dive into key topics and selected opinions.

As usual, we’ve also included a quick-fire update on the latest Basis Markets developments, but head over to the Basis Markets Discord & members-only area for more.

Macro environment

The economic momentum from 2023 has carried over into H1 of 2024, marking another strong period for global markets. In Q1 this was in largely driven by cooling inflation and increasing expectations of imminent rate cuts in the US. Q2 has seen a shift towards more conservative views on cuts, with risks of US economic overheating causing concerns, but hopes for a soft landing persist and central bankers may well be patting themselves on the back.

In Europe, the economy also continued to show positive movement driven by cooling inflation and increased consumer confidence and spending following a period of high inflation.

Inflation remained more stubborn than expected, in many countries particularly in the services sector, staying above central bank targets. This led to the delays in expected rate cuts compared to earlier in the year. Overall, markets remained resilient, buoyed by the easing of initial fears and steady economic growth, although inflation and central bank policies continue to be critical areas to watch for the remainder of 2024.

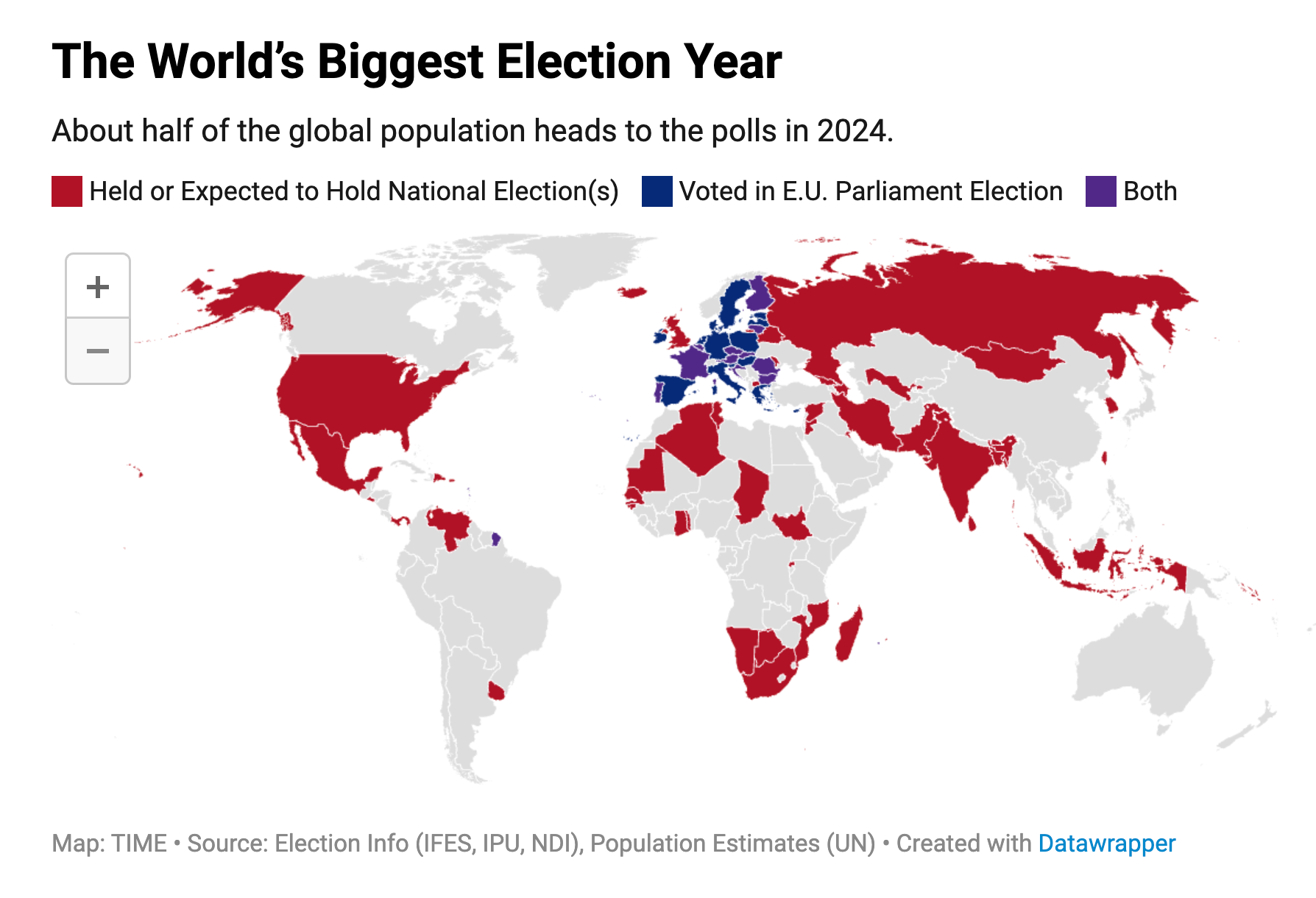

Political uncertainty is another theme of 2024, with 64 elections taking place, representing 49% of the world's population.

Let’s dive into the intricacies of global macroeconomy performance in 2024 so far.

Global indices

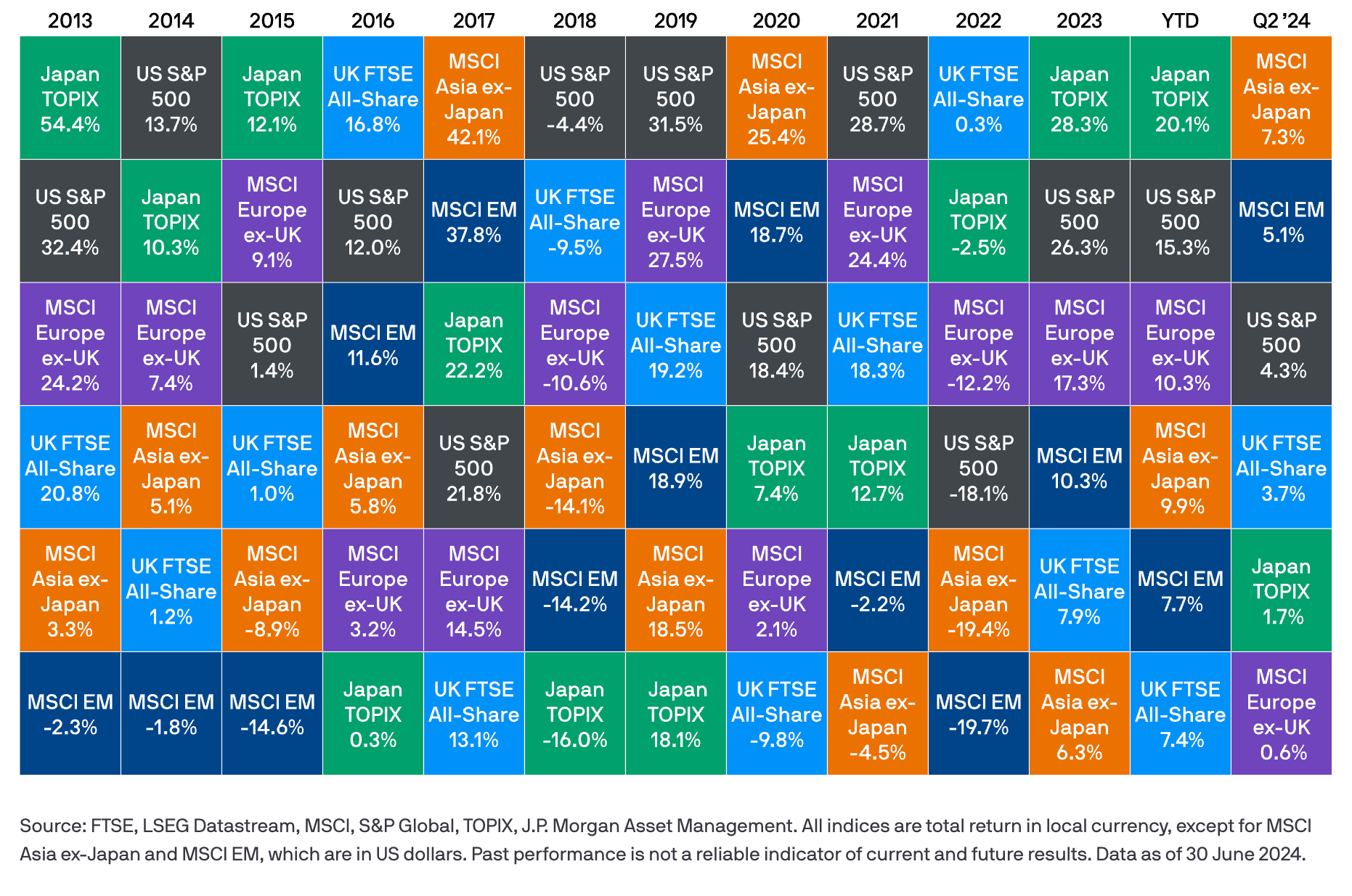

Global stock markets have seen strong returns in 2024 across the board. Whilst the Japanese TOPIX leads the pack year-to-date following an 18% rally in the first quarter of 2024, all eyes remain on the US, which continues to drive returns for globally diversified investors.

A strong US economy provided the backbone for equities optimism, supported by data releases showing economic resilience, including the Q4 annualised GDP growth figure being revised up to 3.5%, Nonfarm Payrolls remaining robust, and the Purchasing Manager's Index signalling expansion.

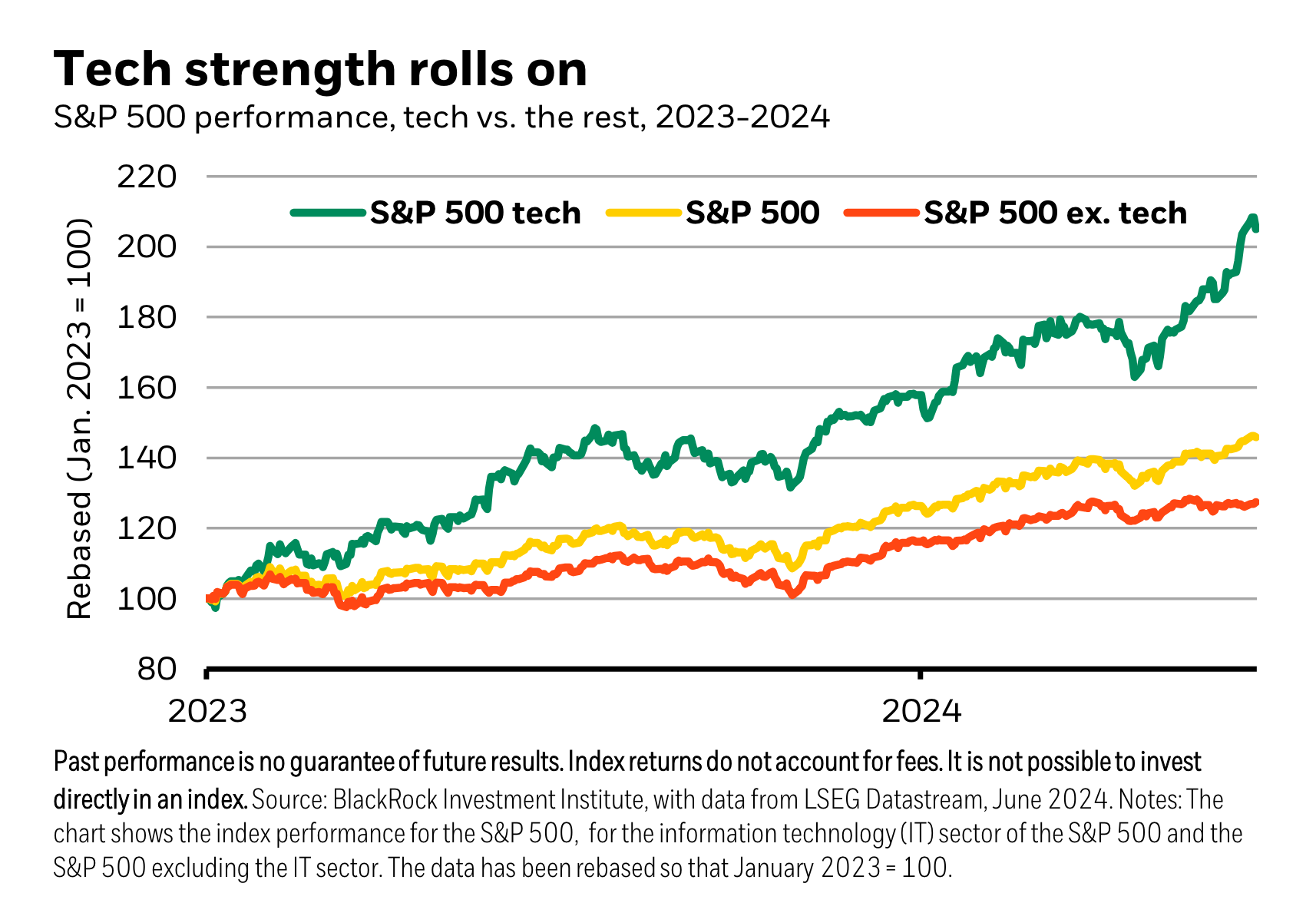

Strong corporate earning and outlook statements have also supported increasing equities valuations, including from some of the Magnificent Seven. This, alongside a theme of continued enthusiasm around Artificial Intelligence (AI) has seen the Technology and Communication Services sectors increase their relative performance and valuations versus the broader market, particularly Utilities, Real Estate, Materials and Industrials.

Overall, the Technology sector has dominated growth and is now up 30% this year and 100% since 2023, with justifications including free cashflows, high profitability and earnings growth.

The AI rally is now broadening from mostly hyperscalers (Amazon, Meta, Microsoft, Google) and semiconductor manufacturers (Nvidia), into other AI connected winners. Companies focussed on build-out of AI infrastructure such as data centres, energy storage and electrification have also posted an impressive average return of 26% year-to-date.

However, there is some caution in the market as revived expectations for rate cuts following June CPI prints could signal a rotation from Large Cap stocks into more rate-sensitive sectors such as Real Estate and Smaller Companies, which rose amidst falls in the Nasdaq in mid-June

Outside the US, strength in Asian markets has helped Emerging Market equities to outperform Developed Markets, reversing the trend. In Europe, strong growth, business activity, and equity performance in Q1 has been hindered by the announcement of parliamentary elections in France and an expected slower pace of rate cuts due to sticky inflation, despite the European Central Bank cutting rates by 0.25% in June. In the UK, the country has recovered from a slight recession in H2 2023, returning to growth this year despite increasing unemployment and an upcoming election. Valuations remain significantly lower than average in the region.

Overall, global indices largely continued the trends from 2023, although a resurgence of Emerging Market Equities, and a potential rotation of assets between sectors and regions could be on the cards.

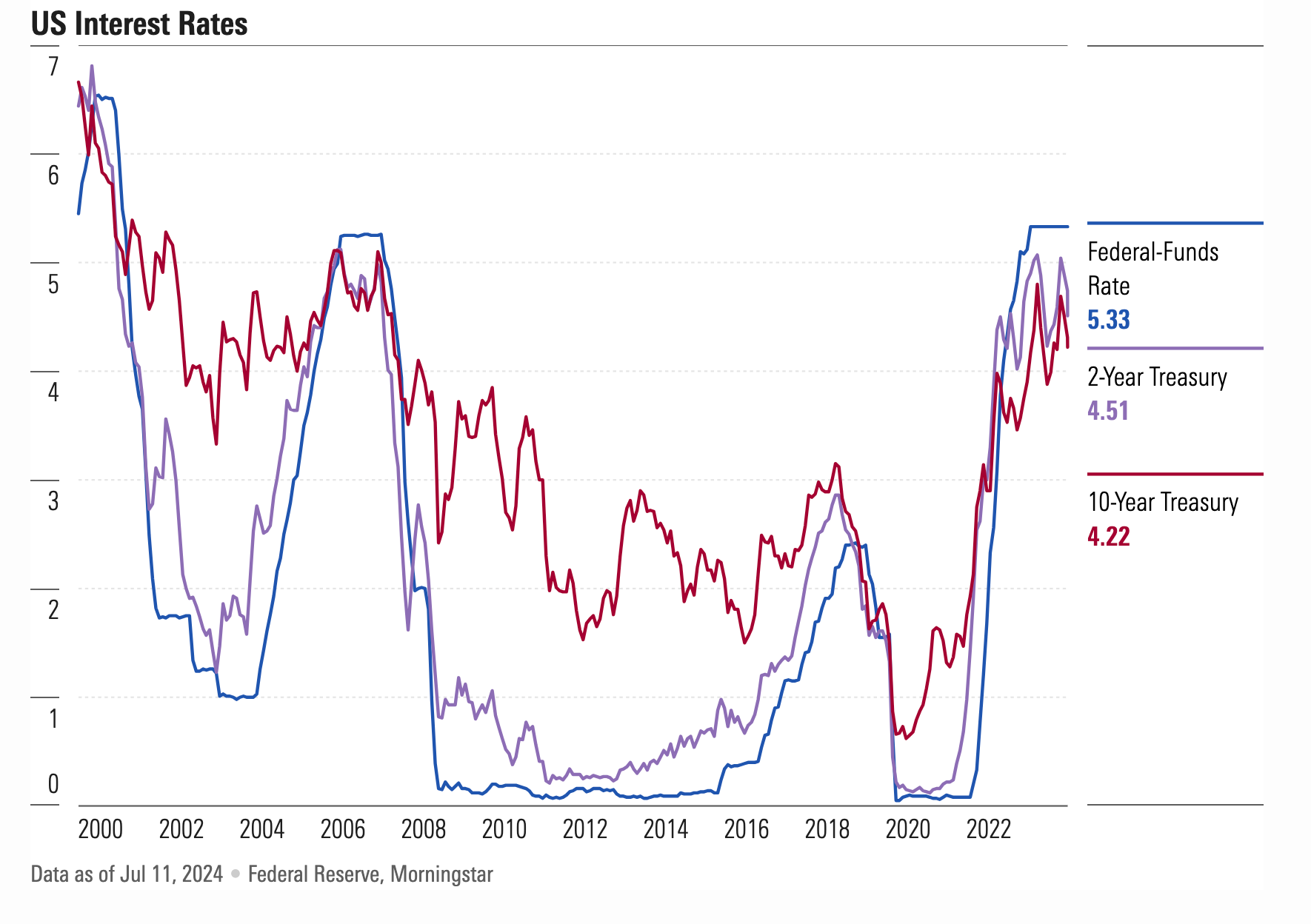

Bonds

With economic resilience comes challenges for the bond market, which have struggled alongside the delayed expectations of rate cuts and questions over persistent inflation, although softer labour market conditions and inflation news have helped ease the pain.

In government bonds, many countries' treasuries followed the broader market, but there were some specific cases of over/underperformance emerged including in France with uncertainty over elections.

Corporate bonds, in particular the high yield sector performed better largely due to earnings which widened credit spreads over government bonds. This has produced absolute and relative positive returns in recent months.

With bond yields so closely linked with interest rates, it's no surprise that long bond markets are eagerly awaiting rate cuts. Let's look at inflation expectations.

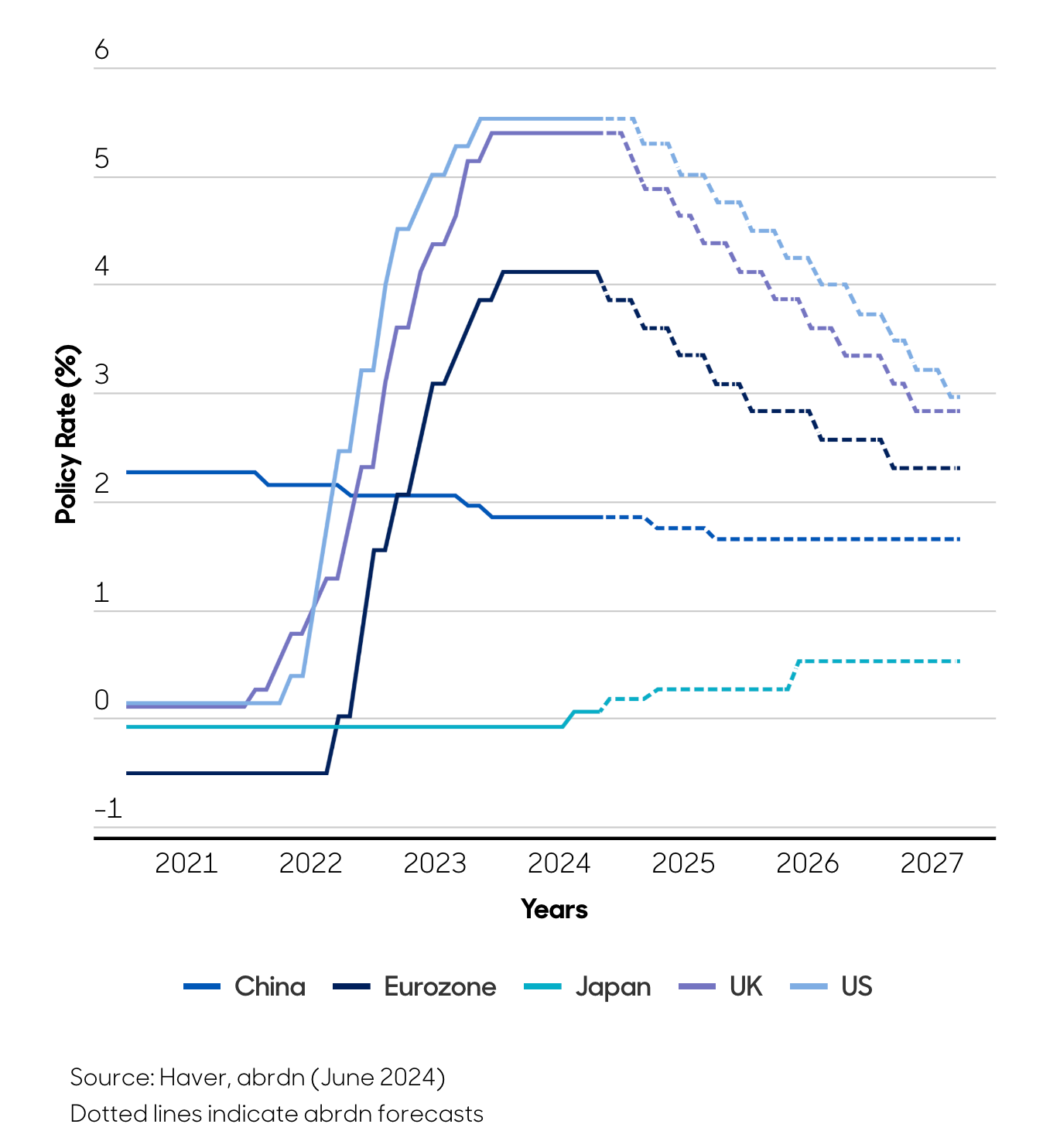

At the start of the year, cuts were expected as soon as March, which shows how much unexpected "stickiness" there has been in inflation. At one point in April, there were even fears of further hikes from some central banks (for a short period). Now, it appears these fears were unfounded and markets are confident that easing monetary policy is indeed the next move for most global economies including the US, where the Fed has hinted about one rate cut coming late in 2024.

Some countries have gone ahead, including the European Central Bank which cut rates by 0.25% in June. In the UK, the Bank of England has reached its 2% inflation target and may cut soon, although sticky services and wage inflation has held them back from cutting rates to date.

Whilst the questions of "when", and "by how much" rates will be cut is uncertain, the futures market imply cuts (in the US) down to a rate of 3.5% in 2026, although some commentators expect much lower.

All eyes will be on inflation prints, the labour market and central banks over the rest of the year.

Commodities

Looking at a broad basket of commodities, performance has been reasonable in 2024 to date, recording 8% growth to reverse the losses of 2023. Performance has diverged between subsectors, with significant gains in precious metals, industrial metals and energy.

Agriculture has been more lacklustre, with 200% growth in cocoa prices in Q1 and increased coffee demand in Q2 not able to offset poor performance from cotton, corn, and sugar.

In Energy, oil demand has been decreasing, with Chinese demand falling consistently in recent months, although OECD demand has been picking up, for example in the Eurozone. Global supply continues to increase, in particular in the US, Canada, Guyana and Brazil, a trend that's expected to continue into 2025.

Crypto markets

Things have changed significantly since this time last year, amidst the dark days of 2023. The Bitcoin price was ranging between $25,000-$30,000 despite upside in equities markets, the total value locked (TVL) in decentralised finance protocols was declining month-on-month with no signs of reversing that trend, and sentiment was low despite positive news events.

Fast forward to 2024, and crypto has regained is place in the limelight as an industry of exceptional note as well as financial performance. BTC has 11 ETFs and today marks the eagerly awaited launch of Ethereum ETFs following approval by the SEC.

Recent months have seen frustratingly lacklustre price movement despite these positive news events such as: record inflows into Spot Bitcoin ETFs; surging open interest for regulated futures contracts; stablecoin volume records; record growth in Ethereum Layer 2 active addresses; DeFi TVL and revenue growth; and even crypto-positive sentiment from your favourite US presidential candidates. However, if we step back and look at 2024 to date in context, this gives a quite different and more positive perspective on performance.

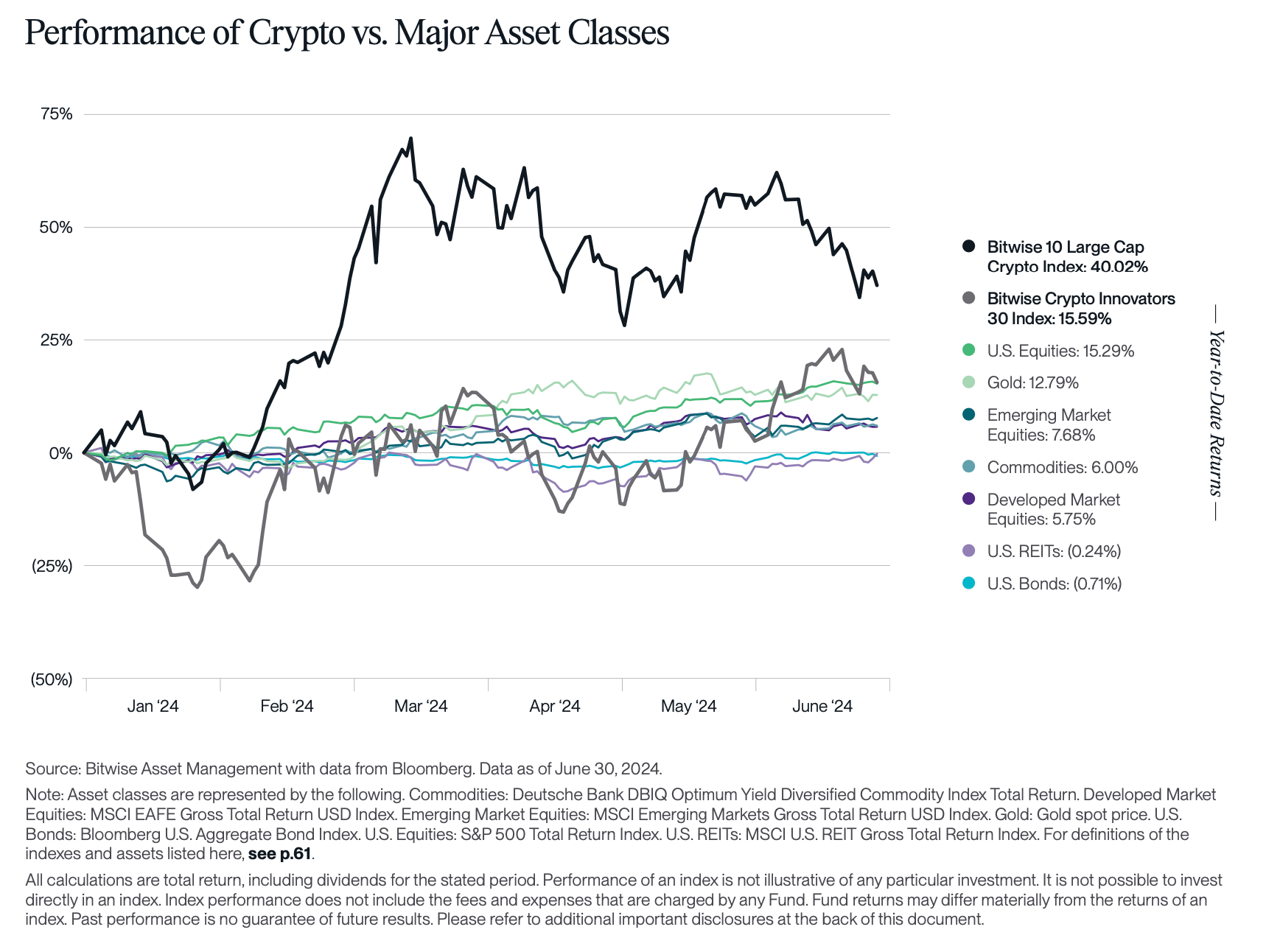

Comparing an index of the top 10 large cap crypto assets to other asset types shows the outperformance over the first half 2024. Behind that, an index of crypto-related equities (think miners and the like) follows, before U.S. equities, gold, and other asset classes. Whilst all assets registered positive gains in this period, the descriptively named "Bitwise 10 Large Cap Crypto Index" registered performance of 40%, well above U.S. equities at 15%. It's easy to see why Bitcoin ETF flows have been so strong ($2.4bn+ in Q2 alone) with this compelling narrative being put to a new audience of investors. In fact, the demand from ETFs alone is outstripping new Bitcoin being mined, putting pressure on supply and uplifting prices.

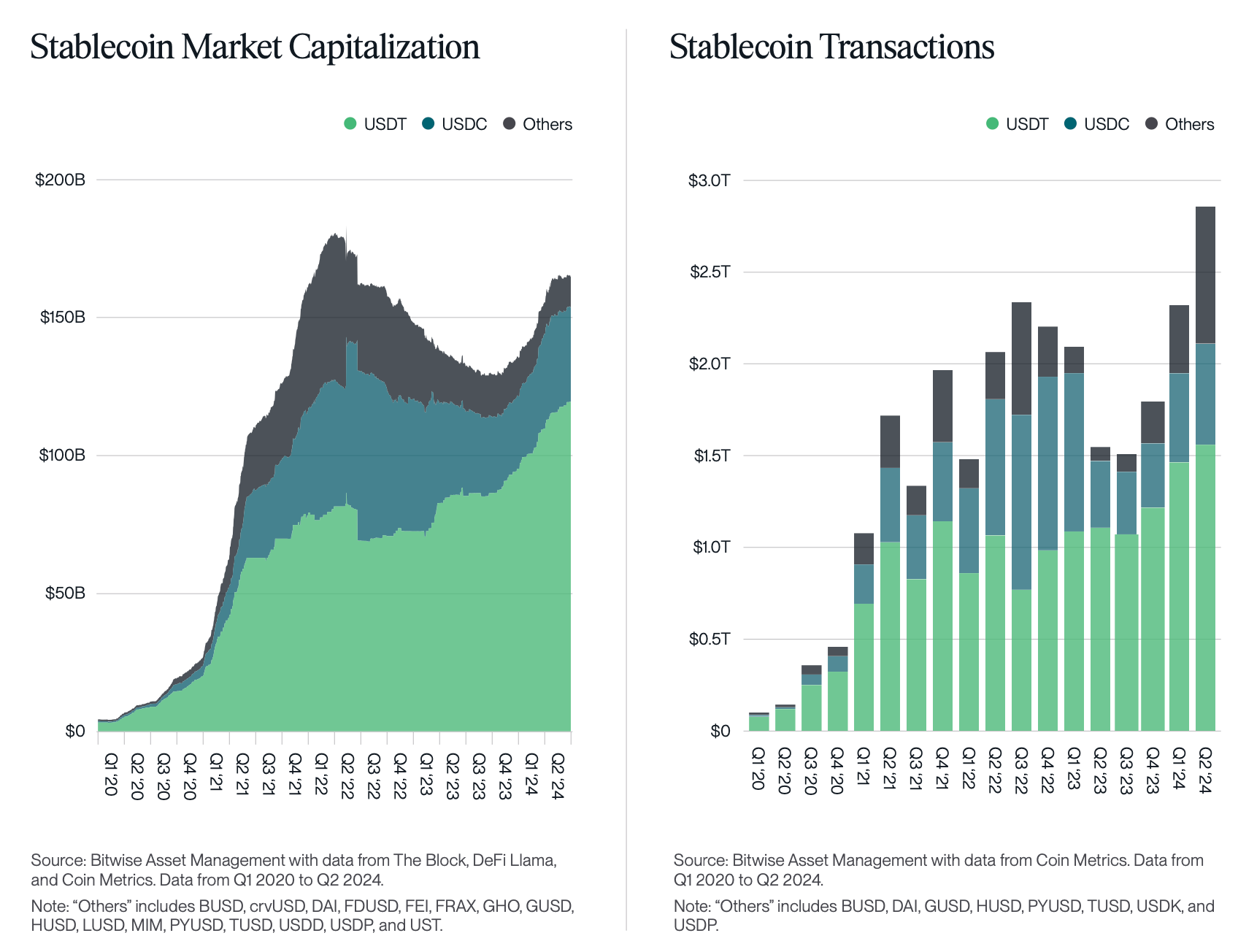

One of the most compelling use cases for crypto is in facilitating fast, efficient, and open payments across the globe. It's interesting to see the growth in stablecoin market capitalisation is increasing, nearly reaching the highs of 2022. In terms of transactions, the growth is even more noticeable, with quarterly transaction volumes at an all time high of over $2.75 trillion.

Crypto markets appear to be in a good place, and with more positive news events to come including Ethereum ETF trading, potential Solana ETFs on the horizon, record numbers of users and developers interacting across many chains, as well as potential political support, it's a great time to be watching the industry evolve.

With high levels of open interest alongside strong trading volumes, there is plenty of opportunity to capitalise by earning yield through delta neutral trading no matter the direction or timing of prices. As is it's mission, Basis Markets continues building towards having the most complete and easy to use tools to understand, explore, and execute on these opportunities.

Follow Basis Markets on X, join the conversation on Discord, and check out project documentation to find out more about the project's forthcoming BTX 1.0 and BTE 2.0 releases.

Crypto market news

A selection of recent news pieces:

- Polymarket trading markets exceeds $500m past as 2024 election enters uncharted territory. Link.

- The total value locked on Solana Defi has increased over 25% in a month, reaching $5.2+ billion. Link.

- Bitcoin mining sector is attracting growing investor interest following high profile AI deal with CoreWeave. Link.

- Bernstein says market has not priced in positive shift in crypto regulations under potential Trump victory. Link.

- Tap-to-earn is the new crypto gaming trend, with Telegram's TON chain shaking up the decentralised gaming industry. Link.

- U.S. spot Ethereum ETFs are due to start trading on July 23. Link.

Feature: Solana in the spotlight

Basis Markets' favourite blockchain, Solana, and the SOL token continue to attract attention from developers, users, investors, gamers, art collectors, and speculators alike. Not only that, the potential approval of a Solana Spot ETF following filings with the SEC could open the chain up to an even broader audience.

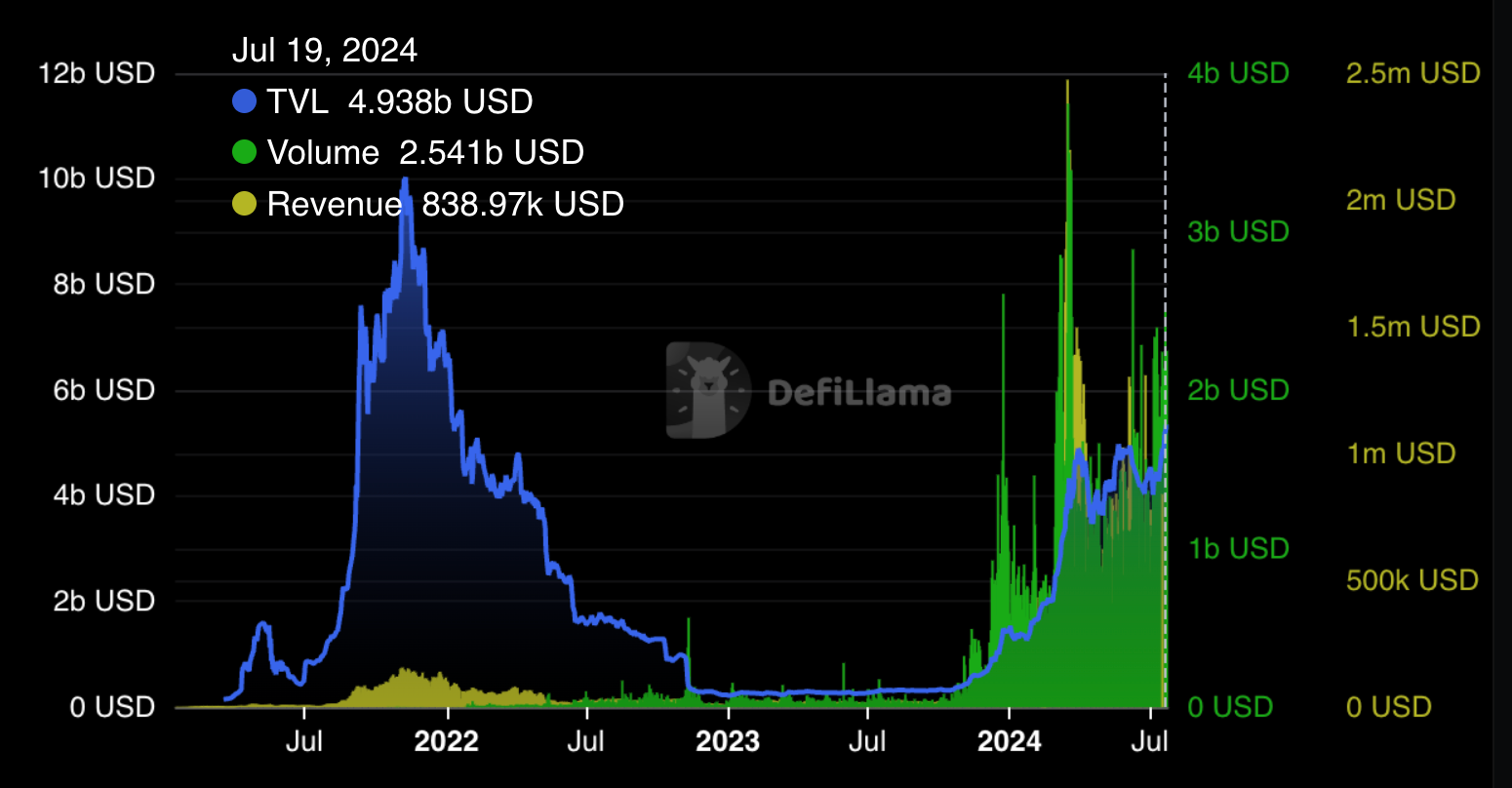

Turning first to the world of decentralised finance, it's clear that Solana DeFi is seeing a significant resurgence, with total value locked hitting $5bn USD. Whilst this is below the peak of 2022, volume and revenue are significantly higher, hovering around $2bn volume and close to $1bn revenue.

Decentralised finance is a core use case of Solana, and fits with the surge in stablecoin issuance as users look to utilise their crypto on Solana protocols. Following its community Airdrop, Jito is the largest, with over $2bn TVL, followed by Marinade and Kamino Finance. The majority of value is locked in Liquid Staking and Staking Pools, followed by Lending , Liquidity Management, Decentralised Exchanges and Derivatives (e.g. Jupiter, Drift).

If momentum continues, the Solana DeFi market could see TVL reaching all time highs before long, especially if expectations around future Solana ETFs remain positive.

Investment firms VanEck and 21Shares kicked off a first wave of filings with the SEC for potential future Solana ETFs. Similar to the hype seen with Bitcoin ETFs, there is hype around a potential ETF boosting institutional interest, prices, and liquidity. Already, deily transactions on Solana seem to have responded with an uptick last month.

The approval process is not quick, and a decision from the SEC is expected by March 2025, although with the U.S. election process underway there is increasingly positive political sentiment around crypto, and there is potential for a streamlined process (avoiding the need for an existing futures market).

You can read a more detailed analysis at this link.

Watch this space...!

DAO updates

Recent developments within Basis Markets include:

- BTX multi-exchange enablement: Multi-exchange execution went live in v0.5.0-beta, built on a resilient abstraction layer for seamless cross-exchange operations. featuring KuCoin and Bybit as well as Binance. Improvements are made via regular releases, read more about v0.7.0-beta, with a video of the real-time execution in practice, on X here.

- BTX integration push: Additional exchanges continue to be added to the data pipeline, as well as to the execution engine. WOO X has been the most recent addition to the suite of execution-enabled exchanges.

- BTX & BTE UI/UX overhaul: Significant progress has been made towards a new design system and user interface for the BTX and BTE. You may have seen from some sneak peeks released in the Discord members-only area and on X 👀.

- Data pipeline & infrastructure enhancements: The backend of the Basis Markets tooling has had significant improvements, including integration of data collection and analysis across the two products.

- BTE Re-launch preparation: Development attention is also focussed on preparing for the re-launch of the BTE as version 2.0, with additional features, speed, and insights.

- Continued user engagement and testing: Regular feedback and iteration within the NFT Holder community has been vital to fixing bugs and adding features.

- Continued communications: Comms have included regular engagement in Discord and on X, as well as the return of regular "Townhall" sessions, which share updates across all angles of the project: development, DAO, community, and growth.

Next steps include a continued development push as well as a refresh of the roadmap and advanced planning for the launch of the BTX 1.0 and BTE 2.0.

How to get involved

If you’d like to hear more frequent updates and keep up to date with upcoming developments, please join us in the Basis Markets Discord.

NFT holders can access the members-only area of the Discord, which is where most of the discussion takes place. Here they can find more detail on the development of the BTX, get involved in product-related discussions, and contribute to the DAO. Not only this, NFT holders can take part in the beta release of the BTX and will soon be able to access the BTE 2.0.

Find out more about how to get access by holding an NFT over in the Gitbook.

Thank you

That wraps up this Macro & Markets Snapshot. Hopefully you've learned something new about the recent macroeconomic landscape, crypto market dynamics, and the latest developments within the Basis Markets ecosystem.

Please get in touch if you would like to suggest topics to cover in future Macro & Market Snapshots, and do join us in the ongoing conversation over in the Basis Markets Discord.

Thank you for being a part of the Basis Markets journey as we continue work towards becoming the best place for finding and capturing delta neutral yield.

Disclaimer

Please see the Basis Markets Terms of Service for full details.

NO INVESTMENT ADVICE: The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our Site constitutes a solicitation, recommendation, endorsement, or offer by Basis Markets DAO or any third party service provider to buy or sell any securities or other financial instruments in this or in in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.

All Content on this site is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in the Site constitutes professional and/or financial advice, nor does any information on the Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. Basis Markets DAO is not a fiduciary by virtue of any person's use of or access to the Site or Content. You alone assume the sole responsibility of evaluating the merits and risks associated with the use of any information or other Content on the Site before making any decisions based on such information or other Content. In exchange for using the Site, you agree not to hold Basis Markets DAO, its affiliates or any third party service provider liable for any possible claim for damages arising from any decision you make based on information or other Content made available to you through the Site.

INVESTMENT RISKS: There are risks associated with investing in securities. Investing in stocks, bonds, exchange traded funds, mutual funds, and money market funds involve risk of loss. Loss of principal is possible. Some high risk investments may use leverage, which will accentuate gains and losses. Foreign investing involves special risks, including a greater volatility and political, economic and currency risks and differences in accounting methods. A security's or a firm's past investment performance is not a guarantee or predictor of future investment performance.