Macro & Market Review: Economic & Crypto Analysis & DAO Updates

Welcome to the latest Macro & Market Snapshot from Basis Markets.

Here, we'll dig into the global macroeconomy, asset markets and the crypto industry, as well as a spotlight on China's stimulus package and Basis Markets updates. This section contains a quick summary of what you can expect.

In asset markets, the recent quarter has seen healthy returns across most major classes, despite several bouts of market volatility, including an unnerving dip in early August due to a combination of weaker US economic data, an interest rate hike from the Bank of Japan and thin summer liquidity.

However, the long-anticipated start of many central banks' rate cutting cycles (with the Fed in September), along with positive economic readings on inflation and unemployment as well as new stimulus in China supported markets to recover quickly, pointing to resilient fundamentals such as earnings and multi-month momentum. Read on for more about individual assets and regions.

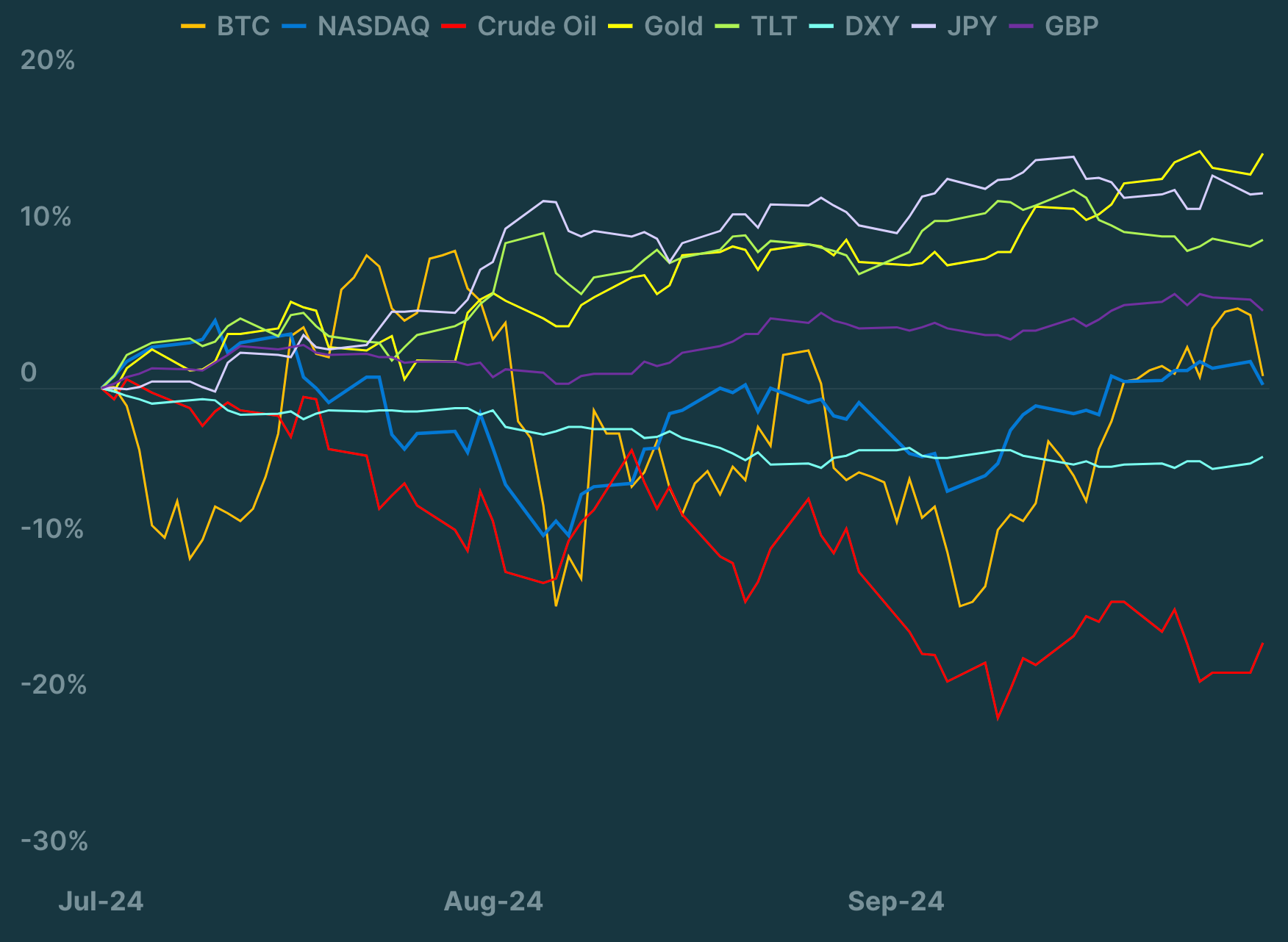

This volatility was reflected in crypto markets, where Bitcoin saw a peak-to-trough fall of nearly 30% in a week, although prices since recovered to their former levels and, on a monthly basis, are still within the approximate $55k-70k range that has persisted since March. However, this certainly does not mean crypto markets have been boring! Volatility leads to opportunities, including basis and other delta-neutral trades. The industry as a whole continues to move forward at a fast pace, check out the Crypto Markets and Crypto News section below for an analysis and some recent highlights.

The project continues to build and grow its product suite, supported by the DAO community, with significant progress in development, design, and planning the three-stage release approach for the upcoming public release of the Basis Trade eXecutor.

These snapshots are designed to give an insight into the global forces shaping the world of macro, markets, futures and flows right now, as well as a deep-dive into key topics and selected opinions. As usual, we’ve also included a section of updates on Basis Markets developments, but head over to the Basis Markets Discord for more & access the members-only area for full updates.

Macro environment

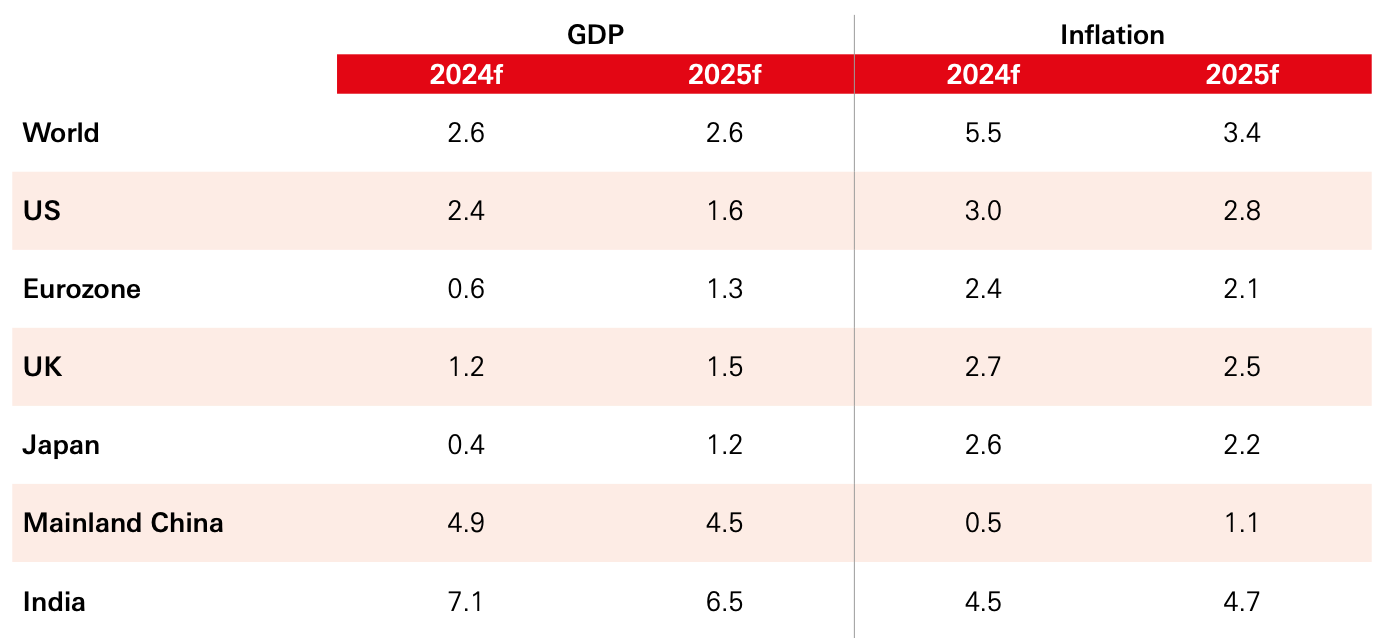

The third quarter of 2024 saw a mixed but resilient global economy. Despite lingering inflationary pressures, especially in the services sector, growth continued across key regions like the US and Europe. The Federal Reserve and other central banks continued their cautious approach, focusing on taming inflation while maintaining economic stability. Although inflation had cooled in most developed markets, it remained sticky in some areas, particularly in the Eurozone and parts of Asia.

The Federal Reserve’s move to begin cutting rates in September brought some relief to markets, which had been anticipating this shift throughout the year. However, uncertainties about the US fiscal outlook and rising global debt levels kept some investors on edge. China's underperformance also weighed heavily on sentiment, with growth forecasts downgraded throughout the year.

Globally, the outlook remained cautiously optimistic, with economies showing resilience despite a volatile geopolitical landscape and persistent inflationary concerns. Let’s jump into the details.

Regional trends

The US remained a stable leader of global economic growth, with the labour market remaining strong and consumer spending holding up well despite inflationary pressures. The long-anticipated rate cuts in September were a key moment, boosting investor confidence and supporting a continued rally. However, some people have concerns that the US economy is entering a late-cycle phase, with rising fiscal deficits and geopolitical tensions adding pressure to both economic growth and market performance.

Europe experienced modest economic recovery in Q3, with energy costs easing and consumer sentiment improving. Germany continued to struggle with its manufacturing sector, but other economies, such as France and Spain, showed stronger-than-expected growth. Inflation remained a key concern, with the ECB being careful and cagey with news of further rate hikes.

Asia presented a mixed picture. Japan showed resilience with positive stock market performance following a rate hike from the Bank of Japan. India, however, continued to be a standout performer, with robust growth driven by strong domestic demand and property market weakness. Despite government stimulus measures in China, growth remained weak, weighed down by property market issues and weak consumer demand, but there are promising signs. Read the spotlight later in this article for more.

Emerging markets, particularly in Latin America, continued to see strong growth, supported by rising commodity prices and stable economic fundamentals. However, as is often the case, political risks in regions such as South America and parts of Asia, are worth keeping an eye on.

Stock markets

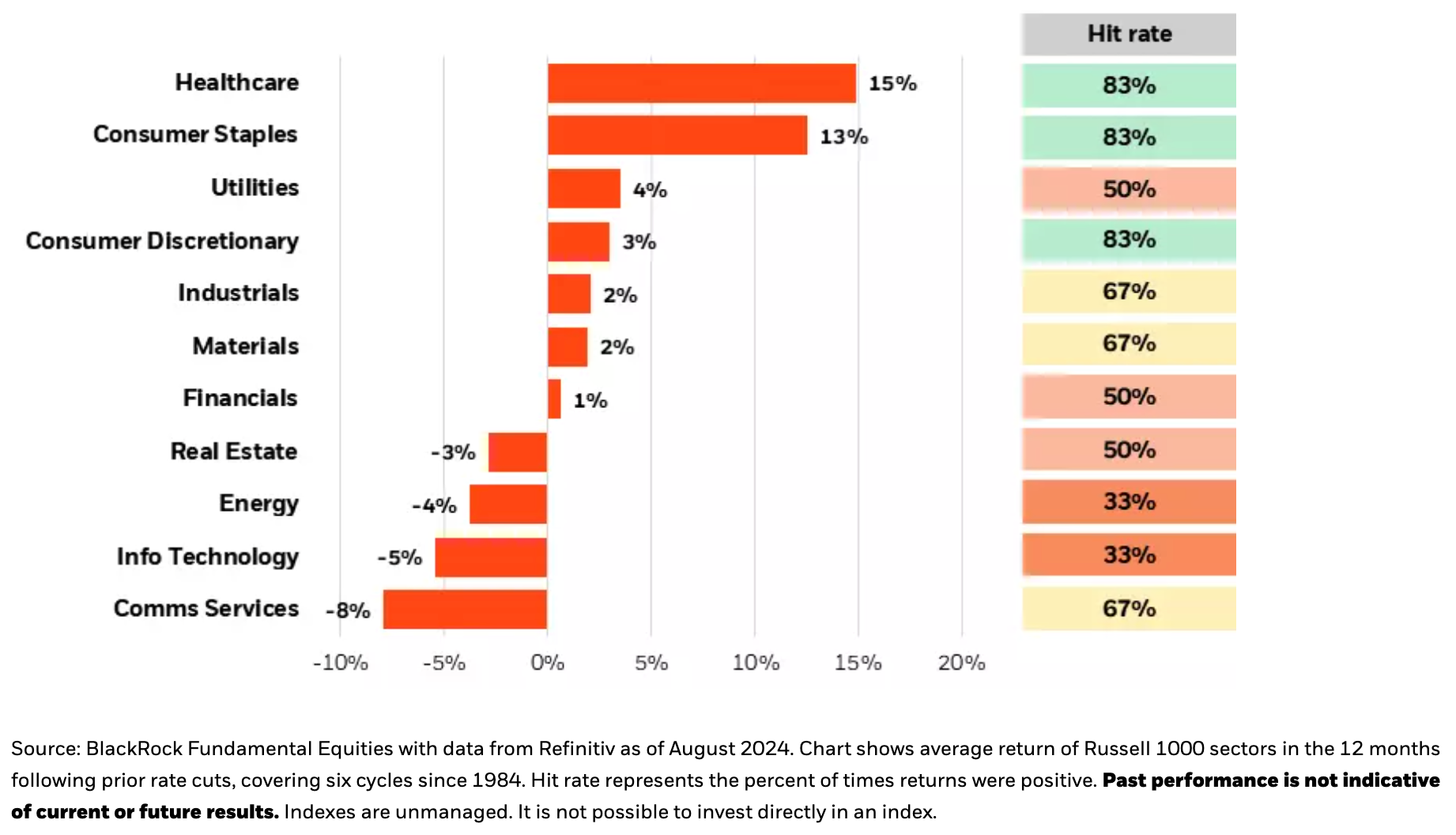

We have seen the broad rally in global equity markets continue, albeit with pockets of volatility in recent months. US equities continued their upward trajectory, led by a strong tech sector, where AI and machine learning remain exciting trends. The S&P 500, closed the quarter with a positive trend, supported by optimism around the Fed’s rate cuts and some strong earnings.

US valuations remain high, particularly in tech stocks, which can be a signal of overpriced assets. However, sentiment is generally positive, for example, based on the charts above and below, which show the average performance of stock sectors following the first central bank rate cut.

European equities did grow as they appear to be emerging from a period of stagnation, although they lagged behind US equities, likely due to Europe's more subdued growth prospects. The region benefited from improving consumer sentiment and reduced energy costs, though inflation remains a concern. Germany, the region's largest economy, continued to struggle with manufacturing sector challenges, but overall market sentiment was supported by the ECB’s cautious approach to rate adjustments.

In Asia, Japan continued to show resilience with the Nikkei 225 benefiting from the Bank of Japan’s rate hike in August, which was seen as a long-overdue move to stabilise its financial markets.

Chinese stocks, experienced sluggish performance to begin with as growth fell below expectations. While the Chinese government's new stimulus measures might not be enough to fully reignite growth, they did provide a short term boost to stock markets. Other emerging markets, led by India, continued to deliver robust growth, with India’s stock market benefitting from its strong domestic demand and stable economic policies.

Bonds

Bonds presented a mixed picture during Q3 2024. After a period of high yields driven by inflationary concerns, bond markets stabilised as central banks began easing their monetary policies. The rate cut in September marked a turning point, bringing some relief to the US Treasury market, though long-term yields remain relatively high due to concerns about rising fiscal deficits.

In Europe, bond markets reacted positively to the ECB’s decision to hold off on further rate hikes, providing a more stable environment for fixed-income investors. However, inflation remaining above target in much of the region, has limited the potential for falling yields and the accompanying price growth. Corporate bonds are performing reasonable well, with investors increasingly looking for yield in a stabilising but cautious macro environment.

Emerging market bonds continue to offer higher returns for investors who are happy to take on higher risk. Countries like Brazil and Mexico saw stronger demand, driven by improving economic fundamentals and declining inflation. However, rising global debt levels and geopolitical risks, particularly in Latin America and parts of Asia, still weigh on the overall market.

Commodities

Commodity markets were volatilein Q3 2024, energy prices in particular. Oil prices fluctuated as OPEC+ maintained its policy of supply cuts, attempting to balance the market amid demand concerns from China and other major consumers. While oil prices remained below their 2022 highs, geopolitical tensions in the Middle East and Africa provided a boost from the lows and are supporting prices.

Gold continued its role as a safe haven for investors, particularly during periods of stock market turbulence, but also saw a large rally rumoured to be due to central bank demand. Combined with central banks worldwide signalling a more dovish stance, demand has pushed gold prices 25%+ higher this year to date. Other commodities like copper and agricultural products faced mixed performances, with various supply chain issues and shifting demand influencing each.

Overall, Q3 2024 presented a cautiously optimistic global economic environment, with resilient stock markets and stabilising bond yields. While inflation showed signs of cooling, it remained a persistent challenge, particularly in Europe and parts of Asia. Central banks began to pivot towards easing monetary policy, which helped to boost market sentiment. However, numerous global elections, geopolitical risks, rising global debt levels, and the uncertain stimulus result in China will continue to shape the outlook for the rest of 2024.

Crypto markets

Looking at the chart below, people would be forgiven for thinking that the past few months has been uneventful in the crypto markets, given the ranging price performance in the past quarter. But this hides a huge amount of news and developments in the industry as it becomes more mainstream and connected within the modern world.

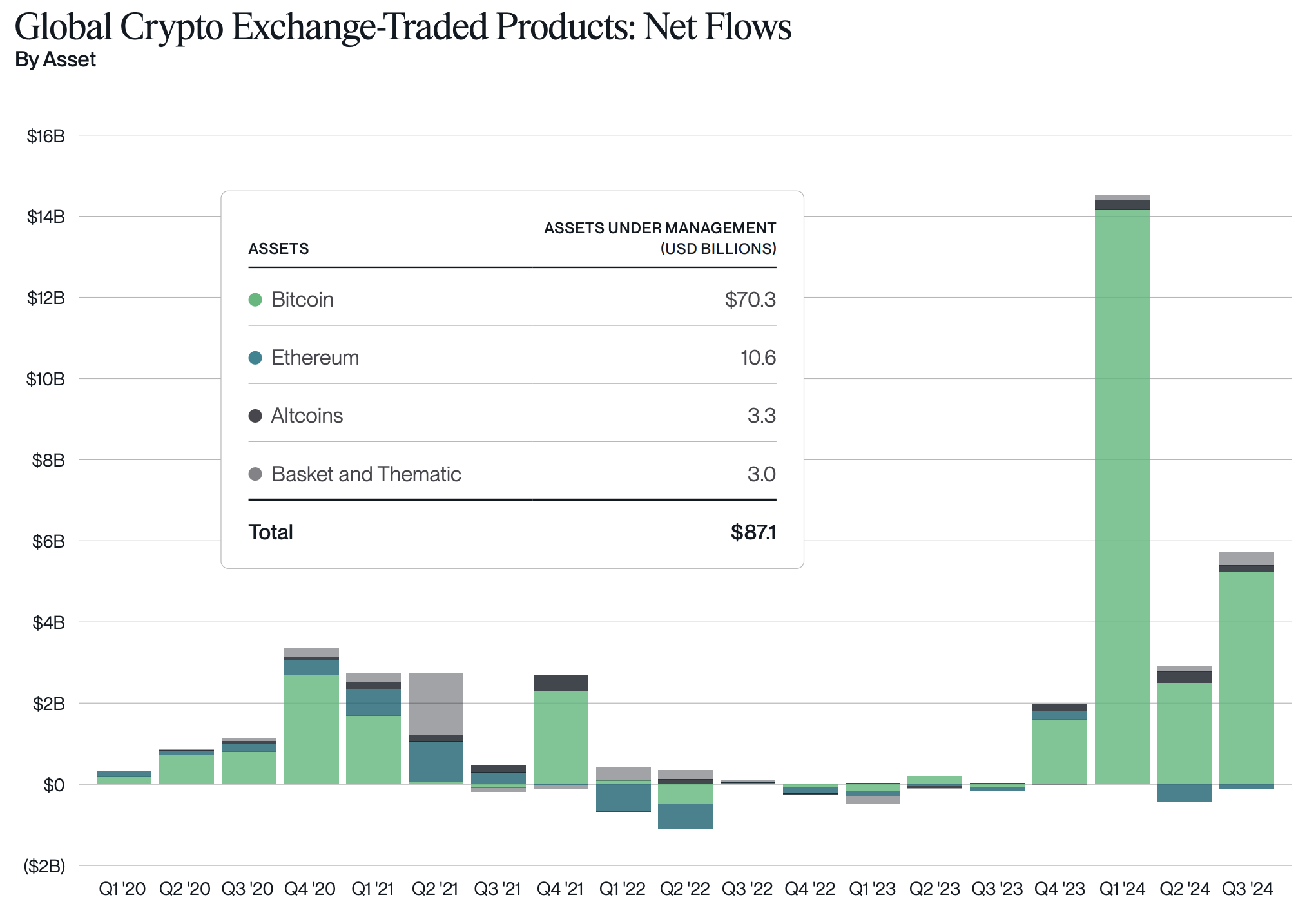

A key theme for 2024 has been integration with traditional markets, and with that, increasing institutional access to the space. This can be seen through the significant inflows into Bitcoin ETFs this year, followed by the launch of Ethereum spot ETFs in recent months. As the Q4 figures in the chart below shows, access to spot ETFs has significantly increased interest in traditional routes to investing in crypto markets.

In a similar vein, regulators appear to be approach digital assets in a more collaborative way, with bodies looking to provide more clear rules, and both US presidential candidates engaging with the space. Also in the US (relevant as the largest market, and one that often leads to other countries following suit), they recently approved the sale and trading of options on Bitcoin ETFs, which is another step in connecting crypto to traditional markets and should lead to higher efficiency in the markets.

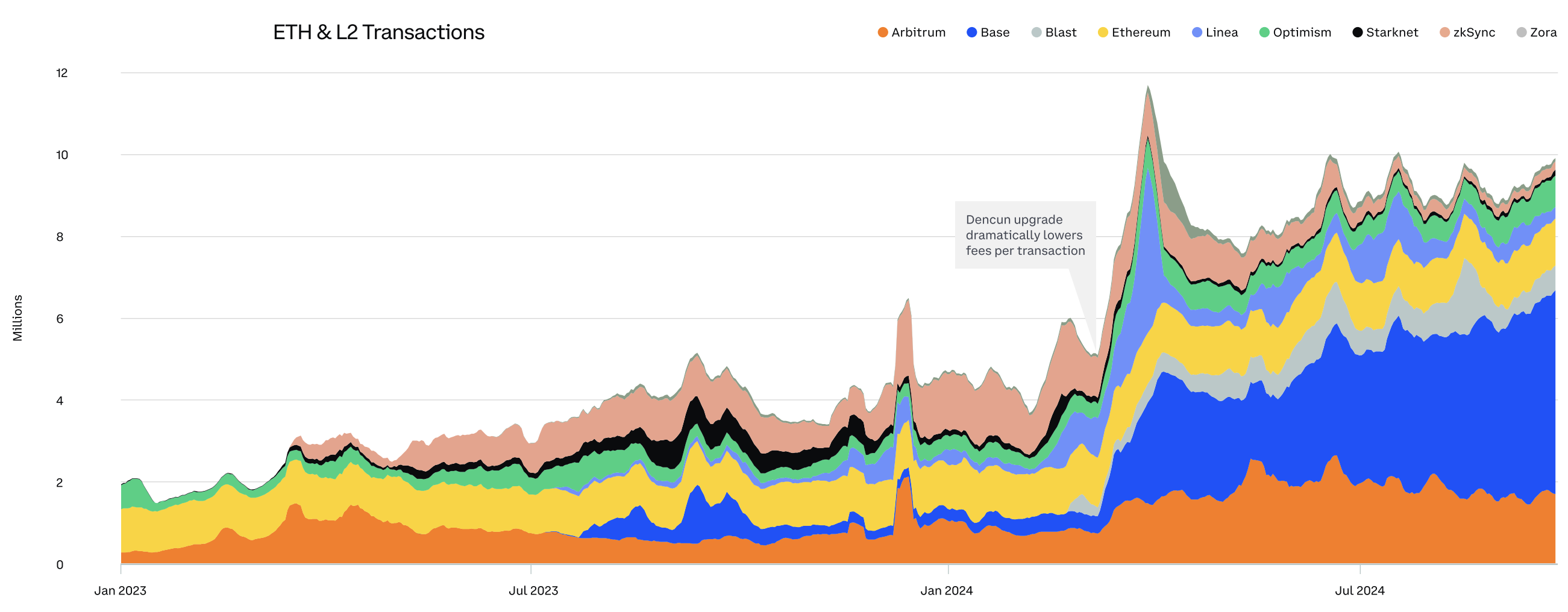

But it's not just traditional routes to crypto which are flourishing. On chain activity continues to surge as users find new opportunities to use crypto, and new use cases. The chart below focusses on Ethereum and the number of transactions directly and via Layer 2s, which have grown more than 5x since the start of 2023.

One example of a thriving use case is in prediction markets, where Polymarket has now broken $1bn in volume. Users make predictions across markets including politics, sports, and business, with $350m+ volume traded on whether Donald Trump will win the US election alone. The mainstream media and even Bloomberg have picked up and integrated data from Polymarkets into their streams.

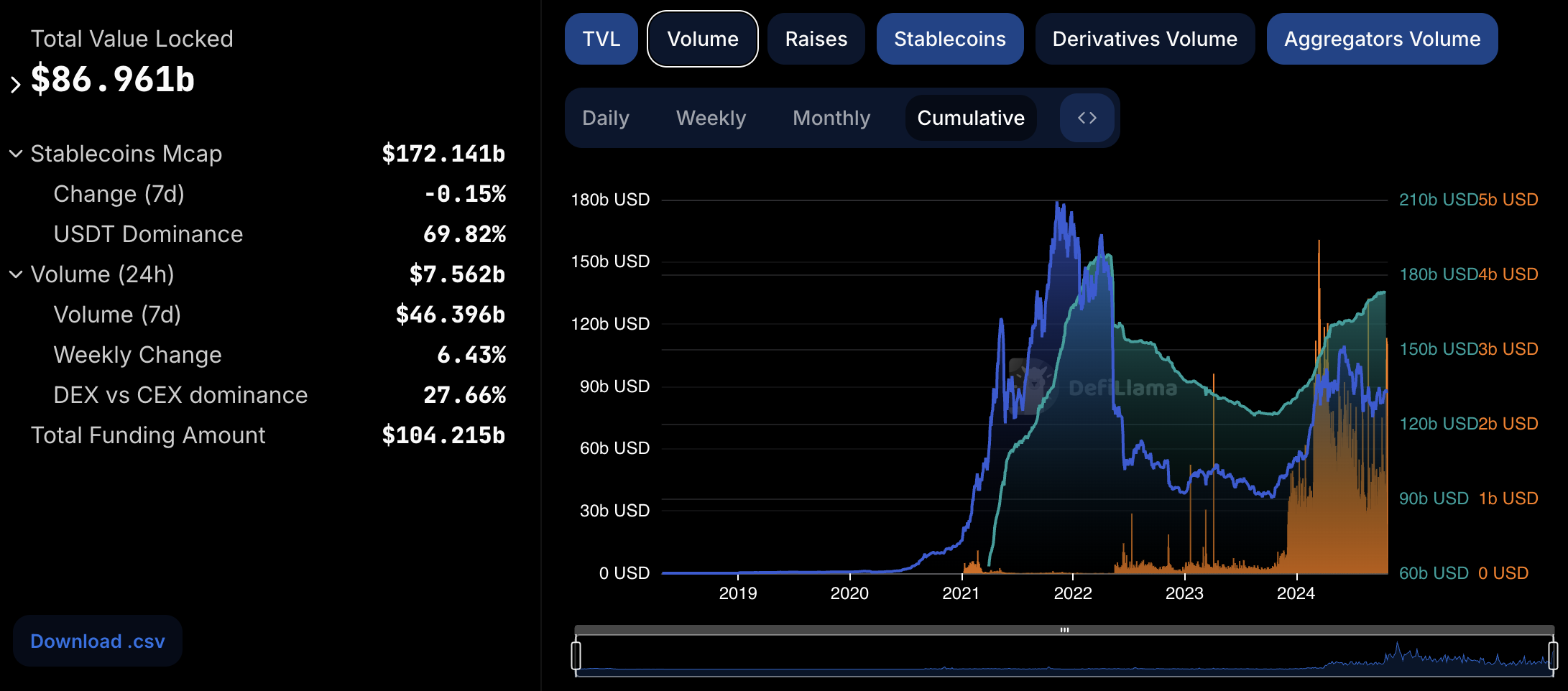

Stablecoin usage is another continuing use case, with stablecoin market cap now over $170bn as institutions realise the scale of the opportunity for increased speed, cost, and security. One example is Stripe's 1$1bn acquisition of the Bridge platform (see the Crypto News section below for more) with the goal of integrating stablecoins within its more traditional payment infrastructure. The trend suggests it's likely we will continue to see growth in this area.

Despite ranging prices, the crypto industry is continuing to develop and grow. As Coinbase summarises this: "markets have grown deeper, more liquid, more sophisticated, and more accessible". Combining this with new use cases and increasing daily active users, there's a lot to look forward to in crypto markets.

No matter the state of crypto markets, there is plenty of opportunity to earn yield through delta neutral trading no matter the direction or timing of prices. As is it's mission, Basis Markets continues building towards having the most complete and easy to use tools to understand, explore, and execute on these opportunities. Follow Basis Markets on X and join the conversation on Discord to keep up to date with the upcoming public launch.

Crypto news

A selection of recent news pieces:

- Tether is 'doubling down' on communication and transparency and is working with regulators, CEO Paolo Ardoino says during a panel on Tuesday at DC Fintech Week. Link.

- Fiat payments giant Stripe has finalised a deal to acquire stablecoin platform Bridge for $1.1 billion to grow its crypto offering. Link.

- Solana's crypto-governance hub Realms starts a new regime with new management and a drive for profit. Link.

- Yuichiro Tamaki, the leader of Japan’s Democratic Party (DPP), proposes reduction in tax rates on crypto gains from 55% to 20% ahead of upcoming general election. Link.

- Solana Mobile introduces its second Web3-focused crypto phone "Seeker" to replace the Saga, launching at $500 for early adopters. Link 1. Link 2.

- The introduction of options on spot bitcoin ETFs is expected to increase volatility and inflows, according to QCP. Link.

- Bitcoin mining difficulty hits new all-time high amid record network hash rate, following halving in April 2024. Link.

Feature: Stimulus in China

China’s recent economic stimulus measures underscore the government’s commitment to addressing slowing growth, targeting sectors like real estate, manufacturing, and tech. This support comes after several quarters of economic underperformance, driven by factors like weak consumer demand and a struggling property sector. Despite these efforts, there are calls for even more substantial fiscal interventions to stimulate broader economic growth.

Reacting to the news, Chinese stocks, reached two-year highs, spiking 25% within days of the meeting, before retreating as nerves set in given the absence of further policy details from officials. Global commodity markets from iron ore to industrial metals and oil also reacted with volatility on hopes stimulus will stoke sluggish Chinese demand.

For crypto markets, China’s stimulus measures could have indirect effects, particularly as China’s performance influences the broader Asian economy, affecting investor sentiment globally.

In the long term, China’s economic policies could also impact the Asian market’s digital asset ecosystem, given the region’s significant trading volumes and strong presence in crypto mining. As liquidity increases in the region, so too could interest in speculative assets, potentially boosting demand for Bitcoin and other digital currencies. However, the Chinese government’s longstanding restrictions on crypto trading limit the direct impact on Chinese investors. Nevertheless, the wider macroeconomic stability resulting from the government's efforts could indirectly benefit global crypto markets by supporting Asian economies and driving more risk-on investment behaviour.

DAO updates

Recent developments within Basis Markets include:

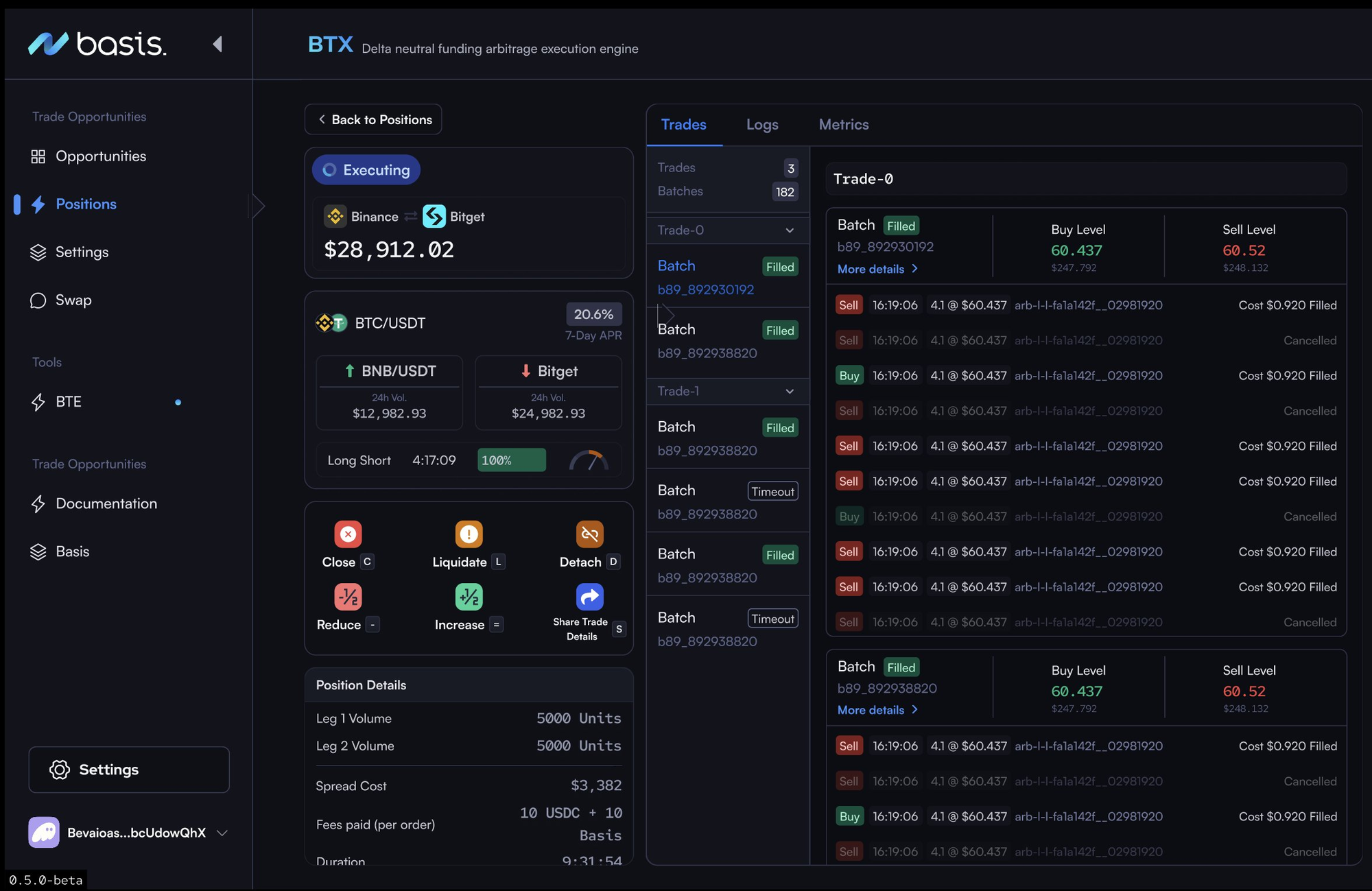

- BTX & BTE UI/UX overhaul: The design team finished work on the latest project, with the new design system and UI/UX for the Basis Markets product suite signed off. This was a huge piece of work with input and feedback from many people across the community leading to a fantastic result. Read more about the process and outputs on X (formerly Twitter) and in more detail on Discord.

- UI/UX integration: The new design system is being implemented into the BTX step-by-step, with significant milestones already reached on areas including the redesigned Positions page.

- BTX multi-exchange enhancements: Additional exchanges continue to be integrated with the BTX, most recently OKX and Bitget, which are now fully integrated and highlighting many new opportunities.

- Trade execution improvements: Hundreds of commits (link) across multiple repositories have brought us closer to the stack required for the public release. The development team has optimised trade execution with fewer orders required, focusing on spread, OI, and other key metrics.

- Ongoing fixes: Building a product suite is never a straight-line process, and the current beta phase has been invaluable in finding and fixing hundreds of bugs, issues, and opportunities.

- User feedback: Beta users have been sharing feedback on their experience with the BTX with some great results. It's been fascinating to hear the different ways people are using the software to support their delta-neutral trading strategies.

- Public launch planning: A proposed roadmap to public launch, colloquially known as the Basis "Launch Trajectory" was shared recently for DAO review, split into a 3-stage process: (1) NFT Full Launch, (2) Invite Launch and (3) Public Launch. More information will be shared about these stages in the near future

- DAO forum: Community members are working to refine the Launch Trajectory, as well as other technical aspects of the tokenomics and release plan. There are DAO proposals potentially coming soon covering these areas so please do get involved, and keep an eye out for updates in the Discord, X and here on the blog for more updates!

A massive thank you to the community members who have gone above and beyond to improve the BTX before it's public release, whether through testing, feedback, discussions, and DAO participation.

Next steps are focussed on the final development sprint towards the go-live of Stage 1 of the Public Launch plan with new features, UI/UX and tokenomics.

How to get involved

If you’d like to hear more frequent updates and keep up to date with upcoming developments, please join the community in the Basis Markets Discord.

NFT holders can access the members-only area of the Discord, which is where most of the discussion takes place. Here they can find more detail on the development of the BTX & BTE, get involved in discussions on the project's roadmap, and contribute to the DAO.

With the public launch drawing ever closer, DAO activity has picked up and there are many ways to get involved and help share the future of Basis Markets. Current topics include planning the final Stages of development releases ahead of the launch phases.

Check out the project documentation for more information about Basis NFTs and their utility.

Thank you

We've come to the end of this Macro & Markets Update. From the macroeconomy to crypto news and the latest developments within the Basis Markets ecosystem, we hope you've found it a valuable read.

Please get in touch if you would like to suggest topics to cover in future Macro & Market Snapshots, and do join us in the ongoing conversation over in the Basis Markets Discord.

As always, thank you sincerely for your support. The community is core part of the Basis Markets ecosystem a the project continues on its journey to being the best resource for delta neutral traders in crypto.

Disclaimer

Please see the Basis Markets Terms of Service for full details.

NO INVESTMENT ADVICE: The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our Site constitutes a solicitation, recommendation, endorsement, or offer by Basis Markets DAO or any third party service provider to buy or sell any securities or other financial instruments in this or in in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.

All Content on this site is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in the Site constitutes professional and/or financial advice, nor does any information on the Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. Basis Markets DAO is not a fiduciary by virtue of any person's use of or access to the Site or Content. You alone assume the sole responsibility of evaluating the merits and risks associated with the use of any information or other Content on the Site before making any decisions based on such information or other Content. In exchange for using the Site, you agree not to hold Basis Markets DAO, its affiliates or any third party service provider liable for any possible claim for damages arising from any decision you make based on information or other Content made available to you through the Site.

INVESTMENT RISKS: There are risks associated with investing in securities. Investing in stocks, bonds, exchange traded funds, mutual funds, and money market funds involve risk of loss. Loss of principal is possible. Some high risk investments may use leverage, which will accentuate gains and losses. Foreign investing involves special risks, including a greater volatility and political, economic and currency risks and differences in accounting methods. A security's or a firm's past investment performance is not a guarantee or predictor of future investment performance.