Slippage: The Silent Killer of Manual Delta-Neutral Trades (And How BTX Beats It)

Slippage kills delta-neutral profits. Learn how it erodes basis/funding trades & how automation like BTX provides the execution edge. Guide.

So, you’re eyeing the delta-neutral game. Basis trading, funding rate farming – it all sounds rather sophisticated, doesn't it? The promise is tantalizing: generate yield, sidestep the market’s mood swings, and perhaps feel just a tad smarter than the HODL-or-panic crowd. On paper, the strategies are elegant. You find an edge – a juicy funding rate, a nice basis spread – set up your hedged position, and then, theoretically, let the market’s mechanics do the work.

It’s a beautiful theory. The delta-neutral dream.

But then there’s reality. And reality, especially in the razor-thin margins of these strategies, has a nasty habit of introducing friction. The biggest, most insidious piece of that friction? Slippage. It’s the grit in the gears, the phantom tax on your trades, the silent killer that can bleed your P&L dry before your strategy even gets a chance to breathe. For delta-neutral traders, slippage isn't just an annoyance; it’s often the difference between a winning strategy and a whole lot of wasted effort.

Edge Erosion

How Slippage Devours Your Trading Profits

Expected Profit Edge

After Slippage Impact

What Exactly IS Slippage? (The Unseen Cost)

Slippage is the difference between the price you thought you were going to get when you hit "trade," and the price you actually got. Simple, right?

You see Bitcoin flashing at $100,000. You slam the buy button. Your order fills at $100,030. That $30 gap? That’s slippage. It’s a direct, immediate hit to your entry cost. It’s the market saying, "Nice try, but the price for admission just went up." It’s the crypto equivalent of that online concert ticket that magically inflates with "service fees" just before you pay – an unseen cost that just is.

What conjures this phantom menace? A few usual suspects:

- Latency – The Millisecond Thief: From your brain to your finger, your finger to the mouse, the mouse click through the internet ether to the exchange’s matching engine… time passes. Milliseconds, sure, but in crypto, milliseconds are eons. Prices don't wait for your signal to catch up.

- Volatility – The Market’s Mood Swings: Crypto isn’t known for its Zen-like calm. Prices whip around. The more they jump while your order is in transit or sitting on the book, the higher the chance you’ll get filled at a price that’s drifted from your initial target.

- Order Book Depth (or Lack Thereof): Think of the order book as a lineup of buyers and sellers at different price points. If you want to buy a chunk of an asset, and there aren't enough sellers at the best price, your order starts climbing up the "ask" ladder, gobbling up offers at progressively worse prices. This is "walking the book," and it’s a prime cause of slippage, especially for larger orders or less liquid assets.

- Your Order Type – The Choice of Weapon:

- Market Orders: The "get me in NOW" button. You get speed, but you sacrifice price. The exchange fills you at the best available prices, whatever they may be. Highly susceptible to slippage.

- Limit Orders: You name your price. "I will buy at $X or better." This protects against price slippage if it fills. But if the market zips past your limit, you’re left on the sidelines, order unfilled, opportunity missed.

What Causes Slippage?

The Four Key Factors That Erode Your Trading Profits

Execution Latency

Time delays between order placement and execution allow prices to move against you

Market Volatility

Rapid price movements create wider bid-ask spreads and unpredictable fills

Order Book Depth

Shallow liquidity means large orders consume available volume at desired prices

Trading Volume

Low volume periods reduce available counterparties and increase price impact

The Slippage Equation

Higher Latency + Increased Volatility + Shallow Depth + Low Volume = Maximum Slippage

Understanding these factors helps traders choose optimal execution timing and strategies.

These gremlins are always lurking. But for delta-neutral strategies, they’re not just lurking; they’re actively hunting.

Why Slippage is Kryptonite for Basis & Delta-Neutral Trades

Slippage is bad for any trade. For delta-neutral strategies? It’s a death warrant. Here’s the grim math:

- The Razor’s Edge Problem:

These strategies are built on capturing tiny efficiencies. The basis spread you’re targeting might be 0.1%. The funding rate might offer a 15% APR, which translates to a minuscule percentage per funding period (e.g., 0.01% to 0.03%). Your profit margins are inherently thin. There’s very little "fat" to absorb unexpected costs. Slippage is a direct cut into that lean muscle. - The Two-Legged Monster:

This is where it gets particularly brutal. A basis trade isn't one order; it's two – a long spot and a short perp, or two opposing perps. And here’s the kicker: you get to experience the joy of potential slippage on both legs. It’s like getting taxed twice. You might get a slightly worse price on your spot buy and a slightly worse price on your perp short. Each hit compounds the other. - Real Impact – Let’s Quantify the Carnage:

Abstract numbers are one thing. Let’s see what this looks like in your P&L.

Imagine you spot a basis trade:- Target Basis Capture: 0.15% (Perp is trading 0.15% above Spot).

- Expected Funding APR: A decent 12% (roughly 0.032% per day).

You go to execute manually:

- Slippage on your Spot Buy: A mere 0.04% worse than intended.

- Slippage on your Perp Short: Another "tiny" 0.04% worse.

- Total Entry Slippage Cost: 0.04% + 0.04% = 0.08%

What just happened?

- Your initial 0.15% basis edge? It’s now effectively down to 0.07% (0.15% - 0.08%) before you’ve collected a single cent in funding. More than half your potential basis profit vanished on entry.

- That 0.08% slippage cost is equivalent to roughly 2.5 days of your expected 12% APR funding (0.08 / 0.032 ≈ 2.5). You’re starting nearly three days behind, just trying to recoup execution losses.

The Double Hit

How Slippage Compounds in Delta-Neutral Basis Trades

Net Entry Position Impact

$75

$60

$135

💸 Actual Profit After Slippage: -$110

Trade turns from profitable to losing!

Consider another scenario: the basis is tight (say, 0.05%), but the funding rate is a juicy 25% APR. Your 0.08% entry slippage instantly puts your basis capture into the negative. Now, that 25% APR needs to first dig you out of a hole created entirely by imperfect execution.

This isn't an exaggeration. This is the daily reality for manual delta-neutral traders. That "silent killer" isn't so silent when you look at the numbers.

The Manual Execution Nightmare: Why Your Fingers Aren't Fast Enough

If you’ve ever tried to manually leg into a two-sided delta-neutral trade, you know the feeling. It’s like trying to pat your head and rub your stomach while juggling flaming torches during an earthquake.

- The Speed Mismatch – You vs. The Algo Hordes: Markets move at the speed of light, or at least fiber optics. Your brain-to-finger-to-click pathway? Not so much. High-frequency trading bots and institutional algos are making decisions and placing orders in microseconds. You’re bringing a butter knife to a laser fight.

- The Coordination Catastrophe: Two screens, maybe two different exchange UIs. You hit "buy" on the spot. Frantically switch tabs. Check the quantity. Hit "sell" on the perp. In those seconds, the market hasn't just moved; it’s sprinted, done a little dance, and is now laughing at your attempt to catch it. Getting the exact same underlying asset price for both legs is a Herculean task.

- The Market Order vs. Limit Order Casino:

- Manual Market Orders: You YOLO both legs with market orders hoping for speed. You get speed. You also get whatever fill price the market deigns to give you, often much worse than you saw a second ago. Kiss your edge goodbye.

- Manual Limit Orders: You try to be smart. Set precise limits. One leg fills. The other? The market zips past it. Now you’re "legged in" – holding a naked spot long or a naked perp short, completely exposed, your delta-neutral dream shattered. Panic ensues.

Human vs. Machine

The Execution Precision Battle in Multi-Leg Trading

👨💻 Manual Mayhem

BUY

SHORT

-$247

🤖 Automated Precision

BUY

SHORT

- Volatility: The Magnifying Glass of Pain: When the market is really whipping around – often when funding rates or basis spreads become most tempting – all these manual execution problems get amplified. Spreads widen. Liquidity thins out momentarily. Your chances of a clean manual entry plummet towards zero.

It’s not that you’re a bad trader. The issue is that when the task is done manually, is fundamentally misaligned with how these markets operate.

The Psychology Trap: "But I Swear My Fills Are Usually Okay!"

Here’s a fun one. Even if slippage is consistently eating their lunch, many manual traders don’t fully internalize it. Why?

- Confirmation Bias: We tend to remember our wins. That one time you felt like you nailed the entry? It sticks. The nine other times slippage nicked you for 0.05%? Our brains are good at papering over those.

- The Fog of War (and Fills): Exchanges don't exactly scream "YOU JUST SUFFERED 0.07% SLIPPAGE!" at you. You see your position open. You see P&L start to tick (hopefully up). It’s hard to precisely reconstruct what price you intended versus what you got across multiple fills for two different legs unless you’re forensically diligent. Most aren't.

- The "Close Enough" Delusion: Milliseconds are abstract. Fractions of a percent feel small. It’s easy to think, "I was quick, it was probably fine." But "fine" for a directional YOLO trade is disastrous for a delta-neutral edge. The scale of precision required is just different.

Without meticulously tracking intended vs. actual fill prices for both legs of every trade, slippage remains that silent, invisible drain. You just know your strategies "aren't performing like they should."

Enter BTX: Automated Precision Execution

If manual execution is the problem, what’s the solution? Hint: it’s not clicking faster. It’s taking the fallible, slow human element out of the critical execution path. It’s automation built for the task.

This is where the Basis Trade eXecutor (BTX) steps in. BTX isn't about finding you trades (though our other tools help with that); it's about executing the trades you've decided to take, with ruthless precision.

Here’s how BTX tackles the slippage demon:

- Machine Speed & True Simultaneity: BTX talks directly to exchanges (Binance, Bybit, KuCoin, WOO X, and more to come) via APIs. No UIs, no browser lag. When you instruct BTX to enter a trade, it's designed to fire orders for both legs at virtually the same instant. This coordination is something a human simply cannot replicate.

- Optimized Order Placement: BTX isn't just spamming market orders. It employs intelligent logic to work your orders. This can mean breaking down larger trades, understanding order book dynamics, and aiming for the best possible net entry price across both legs, actively working to minimize adverse price movement caused by your own orders. It navigates exchange-specific rules (tick sizes, minimums) so you don’t have to.

- Error Annihilation: Wrong pair? Extra zero on the quantity? Clicked buy instead of sell? Automation eliminates these classic human errors that can turn a trade into a costly mistake before it even starts.

The objective is simple: preserve that tiny edge you identified. Give your strategy the clean entry it needs to actually work.

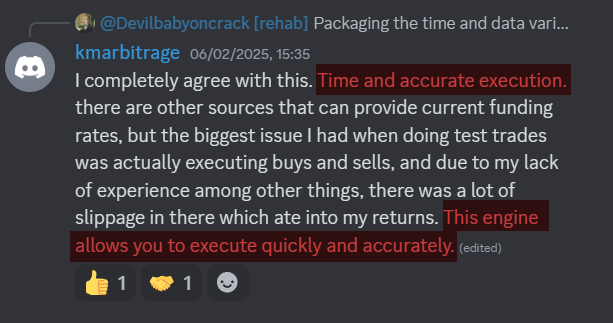

Don't just take our word for it. Here's what a BTX user, previously grappling with manual execution, had to say:

"Time and accurate execution [are important]. There are other sources that can provide current funding rates, but the biggest issue I had when doing test trades was actually executing buys and sells, and due to my lack of experience among other things, there was a lot of slippage in there which ate into my returns. This engine [BTX] allows you to execute quickly and accurately."

That’s the difference automation makes: from "slippage ate into my returns" to "execute quickly and accurately."

Conclusion: Protect Your Edge with Precise Execution

The world of delta-neutral crypto trading offers fascinating opportunities to generate yield by exploiting market structure. These strategies are often elegant in their design. But their Achilles' heel has always been execution. The small edges they rely on are incredibly vulnerable to the "silent killer" → slippage.

Trying to manually coordinate the simultaneous, precise entry of two offsetting positions in fast-moving crypto markets is an uphill battle against latency, volatility, and your own human limitations. More often than not, slippage will claim a significant portion, if not all, of your intended profit before you’ve even settled into the trade.

This isn't a call to abandon these strategies. It's a call to arm yourself appropriately. The Basis Trade eXecutor (BTX) is the specialized tool built to provide that critical execution precision. By automating order placement and optimizing for minimal slippage, BTX helps you protect your edge, transforming delta-neutral trading from a frustrating battle against friction into a more systematic pursuit of identified opportunities.

Because in a game of tiny margins, execution isn't just part of the strategy → it is the strategy.

Ready to start? Grab the Basis NFT (you'll need it to login to the BTX here) and join us at discord.basis.markets for the members only area of the discord where other users share their trades and stories with you.

Feeling overwhelmed? It's easier than it looks. Here's a quick step-by-step on how to get started with the BTX with a simple Long/Short trade.